Ami Organics Limited (after this referred to as ‘The Company’), based in Surat, began as a partnership firm in 2004. The company is coming up with an IPO that opens for subscription on September 1, 2021. Here is all you would like to know about Ami Organics Limited IPO.

- R&D driven manufacturer of specialty chemicals

- Focused on developing and manufacturing advanced pharmaceutical intermediaries for regulated and generic Active Pharmaceutical Ingredients (APIs) and New Chemical Entities (NCEs)

- The company manufactures intermediaries for APIs, including Dolutegravir, Trazodone, Entacapone, Nintedanib, and Rivaroxaban

- Recently acquired ‘Gujarat Organics Limited’. With that, the company manufactures critical starting materials for agrochemical and fine chemicals

- The pharma intermediaries find its application in high-growth therapeutic areas and command significant market share in India and abroad. These include anti-retroviral, anti-inflammatory, anti-psychotic, anti-cancer, anti-Parkinson, anti-depressant and anti-coagulant

- The company exports to various multi-national companies catering to Europe, China, Japan, Israel, the UK, Latin America and the USA. Exports contributed ~52% of revenues in the fiscal year ending March 2021

Ami Organics has developed 450 pharma intermediaries for APIs across 17 therapeutic areas since its inception.

The company operates three manufacturing plants located at (i) GIDC, Sachin, Gujarat, with an installed capacity of 2,460 MTPA, (ii) GIDC, Ankleshwar, Gujarat, with an installed capacity of 1,200 MTPA, and (iii) GIDC, Jhagadia, Gujarat, with an installed capacity of 2,400 MTPA.

Key company strength areas

- Diversified and robust product portfolio duly supported by strong R&D and process chemistry skills

- Wide geographical presence and diversified customer base with long-standing relationships

- Barriers to entry are high in the chemicals industry due to the long gestation period to enlist as a supplier and due to complex chemistries involved in the manufacturing process

- The company has a solid financial profile, with growing revenues and improving margins

- Experienced management team

About the promoter

Mr Nareshkumar Ramjibhai Patel, the promoter, is involved with the company since its inception. He is also the Executive Chairman and Managing Director. A chemical engineer by education, Mr Nareshbhai is responsible for engineering and project implementation.

Mr Chetankumar Chhaganlal Vaghasia, also the promoter, has over 17 years in the chemicals industry. Other promoters are Ms Shital Nareshbhai Patel and Ms Parul Chetankumar Vaghasia.

Financial Profile

Below is the condensed financial information:

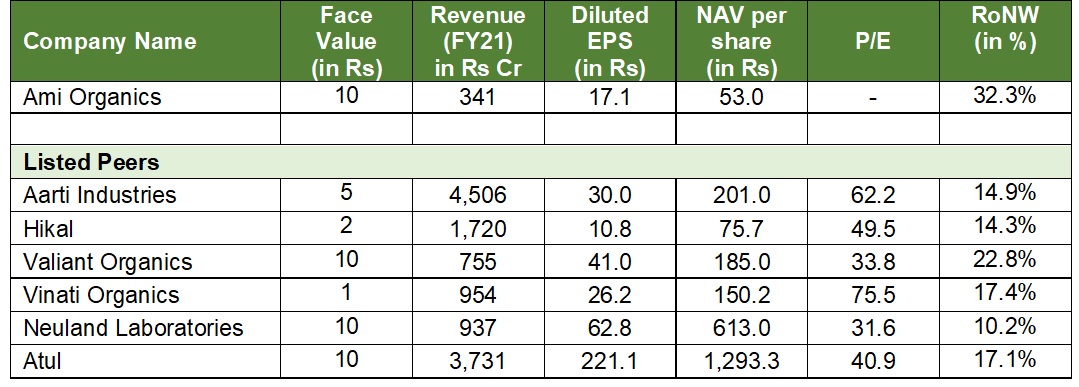

Comparison with other industry peers

The average industry PE is 48.9x

Offer proceeds

| Particulars | Amount |

| Fresh issue | Rs 200.0 Cr |

| Offer for sale (6,059,600 equity shares) | Rs 369.6 Cr |

| Gross issue size | Rs 569.6 Cr |

Utilization of proceeds:

- Repayment/prepayment of certain financial facilities (Rs 140 Cr)

- Funding the working capital requirements of the company (Rs 90 Cr)

- General corporate expenses

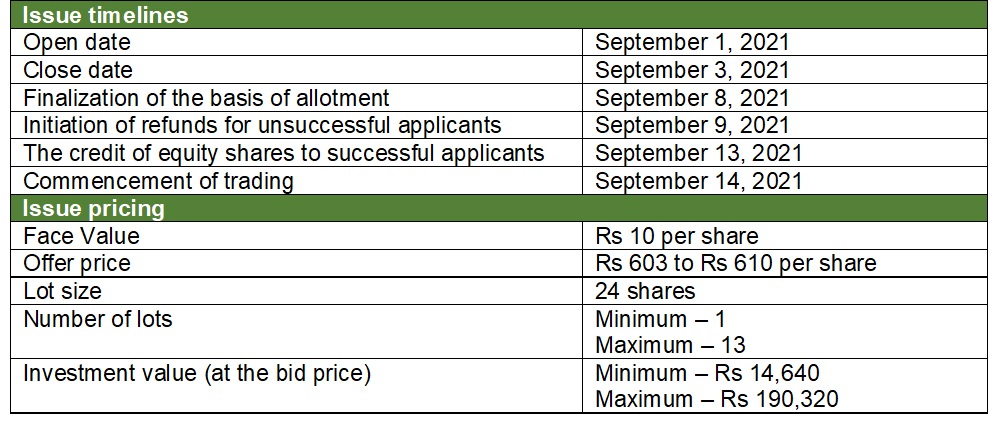

IPO Factsheet

In conclusion

We expect the global chemicals industry to grow robust. Firstly, in the specialty chemicals space, both agrochemicals and pharma-chemicals will be the focus areas. Secondly, several players are opting to diversify their dependence on China. And, China’s loss is going to be India’s gain. In other words, India will grow faster than the industry.

Another reason for the Indian chemicals industry to prosper is the availability of skilled labour at affordable rates. The average monthly minimum wage is the lowest in India amongst comparable countries.

Similarly, the pharmaceutical industry will also grow healthy due to several reasons. These include better healthcare facilities, higher disposable income, raising awareness, higher instances of lifestyle diseases, etc.

At the upper end of the price band, the company P/E will be 35.6x vs the industry average of 48.9x. The company has delivered excellent revenue growth and strong margins. Having said that, fiscal 2021 has witnessed a spurt in revenue growth and EBITDA margin expansion. And, investors may want to remain cautious about the company’s ability to sustain such performance in the future.

There are several reputable and well-performing listed companies in the specialty chemicals space. Therefore, investors have an option to invest in them instead.

In conclusion, we feel that the company is a decent investment opportunity from a long-term perspective. However, investors may choose between subscribing to this IPO (with caution) or invest in an already listed established peer.

The information provided in the red herring prospectus filed by the company with the Securities and Exchange Board of India (www.sebi.gov.in) is the basis for this note. However, I recommend that the reader validate the data before making any financial decision. Also, investment in an initial public offering (IPO) is subject to market risks. Therefore, it should be evaluated, keeping your risk profile and investment objective in mind. The author will not be responsible for any financial loss or otherwise resulting from any action taken based on the above.

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme caution to avoid possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.