Sukanya Samriddhi Yojna (SSY) is a savings scheme to improve the financial independence of a girl child in India. The objective is to encourage families to save for the education and marriage expenses of a girl child. The Government of India launched Sukanya Samriddhi Yojana (SSY) in 2015 as a part of the ‘Beti Bachao Beti Padhao’ campaign.

Here we have discussed salient features of the scheme, operating framework, withdrawal and closure rules, taxability aspect, etc. In short, the article duly elaborates all about the Sukanya Samriddhi Yojana (SSY).

What is the Sukanya Samriddhi Account? Salient features:

- Parents can open the account in the name of a girl child till she attains the age of ten (10) years

- Only one account for one girl child

- You can open an SSY account in post offices or authorized banks

- Account transfer is possible anywhere in India

- Minimum deposit of Rs 250 and a maximum deposit of Rs 1.5 Lakhs in a financial year

- Account deposit is deductible under section 80 C of the IT Act

- Withdrawal to the extent of 50% of the balance is possible to meet the higher education expenses after the girl turns 18. Proof of admission is a must in this case

- The account can be closed when the girl gets married after attaining 18 years of age. Alternatively, the SSY account matures on completion of 21 years from the date of opening the account. However, there is no requirement to deposit between 15 to 21 years, as the payment period is only 15 years

- Interest earned in the SSY account is tax-free. Final withdrawal is tax-free as well

- The girl child can operate the account after she turns 18 years of age

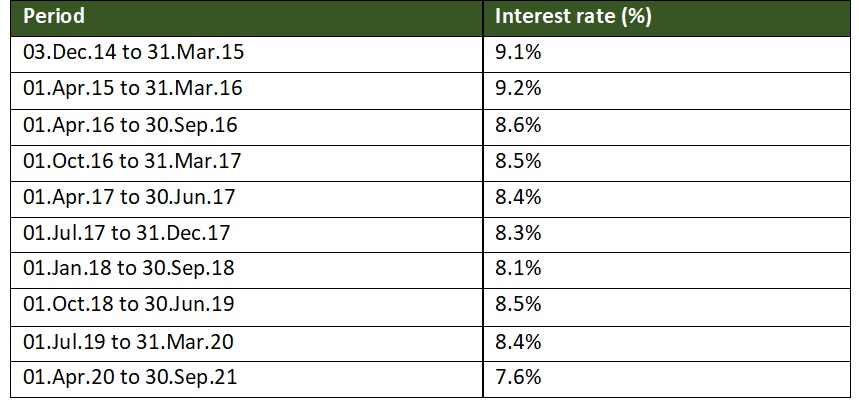

Best in class interest rates

Interest rates under the SSY scheme are best-in-class. The rates have declined in line with the broader market. Nevertheless, despite the reduction, they are still pretty good.

In other words, the SSY interest rates are attractive for the risk-free and tax-free nature of returns.

Rules of interest calculation

As per the rules, the interest gets calculated for each calendar month. It is on the lowest available balance between the close of the 5th day and the end of the month. In conclusion, the interest gets credited at the end of the financial year. Account transfer, in case applicable, does not affect the interest credit.

How does one open a Sukanya Samriddhi Account in any bank?

A guardian can open the SSY account in the name of the girl child, who has not yet attained ten years of age. The age gets calculated as on the date of opening of the account.

An account holder can have a single account under this scheme. In addition, the SSY account can be for a maximum of two girl children in a family. A provision allows adding more than two upon submission of an affidavit supported by birth certificates of twins/triplets. However, the rules clarify that this provision does not apply if first-order birth already resulted in two or more girl children.

Application to open the account must be submitted form in Form-1, along with the birth certificate of the girl child and necessary documents of the guardian (id and residence proof) along with the application.

How does the Sukanya Samriddhi Yojana work? A few ground rules

A minimum initial deposit of Rs 250 is required to open the account. After that, you can make further deposits in multiples of Rs 50. Similarly, a minimum deposit of Rs250 and a maximum deposit of Rs 1.5 Lakhs is possible in a financial year.

If one does not deposit the minimum amount, the account gets classified as under default. However, there is an option to regularize the account subsequently. The regularization is possible by paying a penalty of Rs 50 per day of default and by depositing a minimum annual deposit for each year in non-compliance.

An SSY account accepts deposits until the completion of 15 years from the account’s opening date. The SSY account eventually matures after 21 years from the date of opening. Upon maturity, one can withdraw the balance by providing the necessary documentation – for instance, withdrawal form, proof of identity, proof of residence, age proof, etc.

Premature closure

Premature closure is allowed in the event of marriage. However, the intimation of marriage must be sent a month before or three months after the wedding.

In the event of the death of the contributors, premature closure is possible. In such an instance, you must submit Form-2, along with the death certificate issued by the competent authority.

The accounts officer can approve the closure of the account on compassionate grounds.

In case of a change in citizenship, the account classifies as deemed closed. Similarly, the status also changes in case of a change in the country of residence.

It may be possible that the parent cannot maintain the account due to an emergency medical situation. In that case, the SSY account can be closed prematurely and the amount withdrawn.

Withdrawal

It is possible to withdraw money for the education of the account holder. However, the maximum possible withdrawal is 50% of the account balance at the end of the preceding financial year. This withdrawal is allowed after the account holder has attained 18 years of age or passed the tenth standard, whichever is earlier.

You can withdraw the amount in a lump sum or instalments. In the latter case, a maximum of five instalments is possible and only one per year.

The withdrawal cannot be higher than the actual fee requirement or other charges at the time of admission. Proof of fees gets submitted as a part of the documents.

Closure on maturity

The SSY account matures after 21 years from the date of opening the account.

The account can also be closed early if the account holder submits a request and the reason is marriage. In an upcoming wedding, one must provide a duly signed declaration in non-judicial stamp paper duly attested by a notary. A proof of age that the applicant is not less than 18 years is also mandated. The closure is allowed within the window of 1 month before or three months after the marriage.

Upon application in Form-4, the balance amount with interest is payable to the account holder.

Is Sukanya Samriddhi Yojana taxable at maturity?

One can claim tax benefit to the extent of contributions made to the account. The deduction is available under section 80C of The Income Tax Act, subject to a maximum of Rs 1.5 Lakhs in a financial year.

Interest earned on the account is also tax-free. In addition, the total amount is tax-exempt upon maturity.

This account falls under the EEE bracket, meaning Exempt-Exempt-Exempt. In other words, the investment made, interest earned, and withdrawal are all exempt from tax.

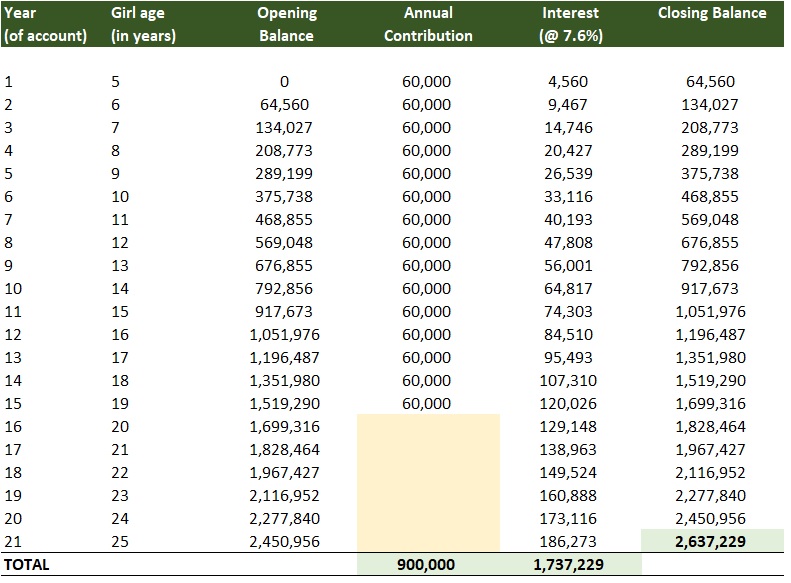

How does the Sukanya Samriddhi Account calculator work?

As per the scheme specifications, we have created an SSY calculator. Here are some of the assumptions we have made:

- The exact amount gets invested each year

- No investment after 15 years (payment period)

- The account is operative until 21 years (maturity period)

- The rate of interest is constant at 7.6% (current rate)

- Annual contributions are made on 1st April every year (once a year)

- No withdrawals done

Based on these assumptions, here is the investment summary:

Key takeaways:

- Principal invested Rs 9.0 Lacs

- Interest earned Rs 17.4 Lacs

- The total amount at the end of year 21 is Rs 26.4 Lacs

- After the girl child age is 18 years, withdrawal is possible. For instance, in year 15 of the account, one can withdraw Rs 7.6 Lacs (50% of preceding year closing balance of Rs 15.2 Lacs)

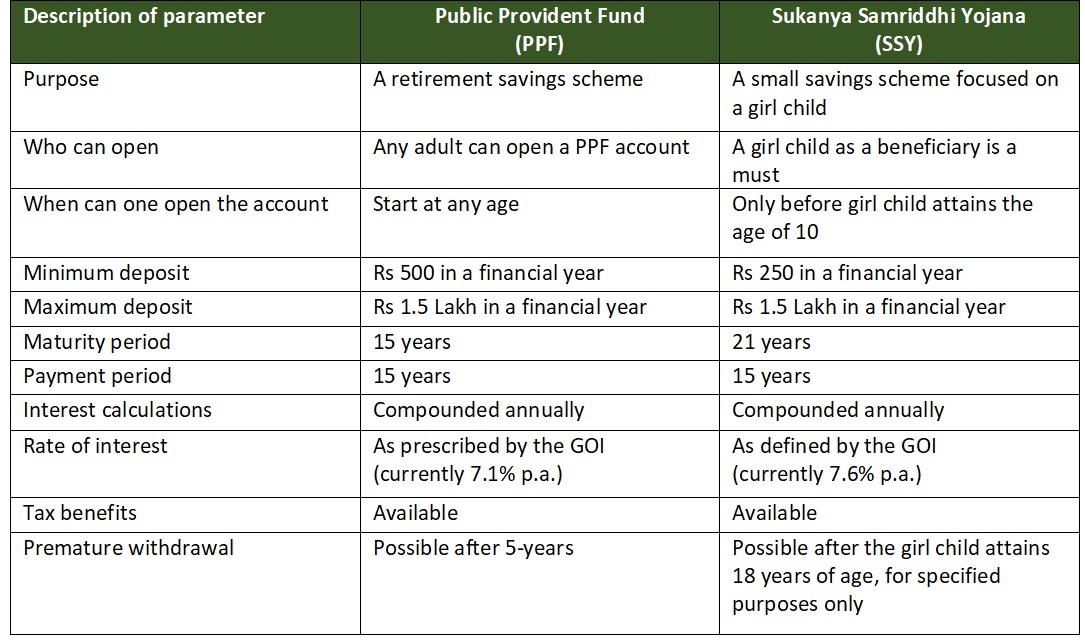

Which is better, PPF or Sukanya Samriddhi Yojana (SSY)?

Amongst others, PPF and SSY are the most popular government saving schemes. However, there are a few fundamental differences between the two.

Which one is better?

To pick one amongst PPF or Sukanya Samriddhi Yojana is very difficult as the purpose is different. However, the above table lays down critical points of difference to help you decide.

In conclusion – is the Sukanya Samriddhi Yojana scheme good or not?

Savings for a child’s future is one of the most crucial objectives for a parent. And parents often go the extra mile to fulfil these needs. There are many options available as long term investment options for a child.

To have a girl child is an overwhelming feeling. So you want to ensure raising her is a happy experience and her future needs are secure. We are referring to the most critical milestones, i.e. her education and marriage. The Sukanya Samriddhi Yojana (SSY) is one of the most popular schemes for a girl child for the right reasons.

SSY is a small savings scheme, and investment can start with a small amount. Moreover, the interest rate is decent for the risk-free nature of returns that the SSY scheme offers. Finally, SSY is fully exempt from tax, and that makes the returns even more lucrative.

Investment options such as equities, mutual funds, currencies, etc., offer better flexibility. For the investors who have access to and understanding these options, SSY may be just one of the options.

Further, there is a long lock-in period, and there are withdrawal restrictions. These limitations exist because the government wants parents to save for a girl child’s education and marriage expenses. Therefore, it is essential to understand the social backdrop of this scheme to appreciate the rules.

In conclusion, the SSY scheme serves a social purpose, offers some flexibility and reasonable tax-free returns. Moreover, the investment is backed by the Government of India, and hence risk-free. Therefore, we believe Sukanya Samriddhi Yojana is a good investment option for the security of a girl child and an option worth considering.

Happy Investing!

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme caution to avoid possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.