Is National Pension Scheme (NPS) a tax saving option or a long-term investment option? There is merit in exploring this question as we believe it is both, but if we have to choose one, it is more of the latter. The National Pension Scheme is an investment tool that focuses on your retirement needs. If the objective is to meet any short term financial goals, then avoid the NPS route.

In other words, NPS is a pension cum investment scheme that acts as a security for the participants. But, on the other hand, NPS is modern compared to old age mechanisms and allows participants to plan for retirement through safe and secure market-based returns. National Pension System Trust (NPST), established and regulated by Pension Fund Regulatory and Development Authority (PFRDA), manages the assets. NPS has become immensely popular amongst investors, as it’s a contemporary investment scheme that merges safety and security with the possibility to modernize the portfolio. Here is all about the National Pension Scheme (NPS).

Essentially, the National Pension Scheme (NPS) is a social security initiative for public, private, and even employees from the unorganized sector.

Who should participate in the NPS scheme?

The NPS scheme is open to any individual who is a citizen of India, aged between 18 and 65 years.

Subject to fulfilment of specific regulatory requirements, even non-resident Indians (NRIs) can participate in NPS. The Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA) prescribes these regulations from time to time.

All the benefits of investing through a systematic investment plan are available through NPS. An investment done so regimentally can make a significant difference to the retirement corpus.

Here are the key features and benefits of the NPS

- The scheme offers market-based returns

- Very minimal costs of investment

- The scheme provides flexibility to choose the fund manager, investment options, annuity service provider, etc.

- Financial experts manage the assets under management, and PFRDA regulates the same

- Investment in NPS provides an additional tax benefit to individuals to the tune of Rs 50,000 per annum

- A participant can start investing with as low as Rs 500/-

- There is a minimum lock-in for ten years; however, this is subject to conditions. In other words, the insistence on long-duration planning is what leads to higher returns

- Technologically advanced NPS allows participants to make contributions online and even track investment performance digitally

- The scheme participants can operate their accounts from anywhere, even if they change cities or employment

What are the different types of National Pension Scheme (NPS) accounts

Essentially there are two types of accounts – Individual NPS and Corporate NPS. Here are some more details:

Individual NPS account

Any citizen of India can enrol under this account and become a participant. The person who gets enrolled is the sole contributor and has complete control over investment in scheme preference. The individual selects the fund manager, the investment option, the annuity service provider, etc.

Corporate NPS account

In this case, a corporate offers an NPS scheme as a retirement benefit plan to its employees under a corporate NPS account. Employees of any corporate registered with the Central Record Keeping Agency (CRA) for NPS can avail of the corporate NPS benefits. With this, both the employee and the employer contribute to the same NPS account. The employer makes a specific contribution (not exceeding 10% of the employee’s Basic + DA) to the employer’s NPS account. The employee also contributes the same amount to the NPS account.

And, then there are two types of accounts, called Tiers, in the NPS terminology. A subscriber has two options to choose from under the same Permanent Retirement Account Number (PRAN). These are:

Tier I Account

Tier I is the main NPS account that operates with the principle of long term savings and offers an additional tax benefit of Rs 50,000 u/s 80CCD (1B). This tax benefit is incremental to the Rs 1.5 Lakh benefit under section 80C of the Income Tax Act. However, withdrawals are restricted under this account and are subject to specific terms and conditions.

Tier II Account

Tier-II account is an add-on account that provides the participant with the flexibility to invest an additional amount. Under this account, an option to withdraw without any exit load exists. However, no tax benefits are available under this account.

NPS offers significant flexibility

NPS offer enough flexibility to its participants, and subscribers have control over the investments made. Therefore, we have listed down the options available to the NPS subscribers. And they must mark their choice during the enrollment process.

Pension Fund Manager (PFM)

There are seven fund managers that PFRDA has appointed, and a participant can choose any one amongst these:

- HDFC Pension Management Company Limited

- UTI Retirement Solutions Limited

- Kotak Mahindra Pension Fund Limited

- LIC Pension Fund Limited

- SBI Pension Funds Private Limited

- ICICI Prudential Pension Funds Management Company Limited

- Birla Sunlife Pension Management Limited

Further, to assist participants in the selection process, the NPS trust website provides the historical performance for each of these PFMs, here is the LINK. As per the existing rules, a participant is allowed to change PFM once in a financial year.

Investment Option

Here, there are two choices – Active choice and Auto choice. If a participant does not select, the funds are invested in the Auto choice mechanism by default. Below are the details for each of the investment options.

Under the Active choice, there are four classes of assets to choose from, and in varying proportions.

- E – Equity and related instruments wherein the allocation cannot exceed 75%. Further, there are some age-wise restrictions on the maximum allocable equity proportion, as mentioned in the table below

- C – Corporate debt and related investment options where the allocation can be to 100%

- G – Government Bonds and associated instruments; can be allocated up to 100%

- A – Alternative Investment Funds where there is a 5% cap to the fund allocation

Here is the equity allocation matrix for active choice investors:

| Age (years) | Max Equity Allocation (%) |

| Up to 50 | 75.0% |

| 51 | 72.5% |

| 52 | 70.0% |

| 53 | 67.5% |

| 54 | 65.0% |

| 55 | 62.5% |

| 56 | 60.0% |

| 57 | 57.5% |

| 58 | 55.0% |

| 59 | 52.5% |

| 60 and above | 50.0% |

However, to form an active portfolio or to decide the allocation may not be a cup of tea for many participants. And, for them, the answer lies in Auto choice. Under this option, the money gets invested in asset classes E, C and G in proportions defined by your age.

The general rule is that one can take more risks at a young age. In other words, as an individual’s age increases, the exposure to equity (riskier asset) is reduced, and in that of government securities (risk-free) is increased. Further, there is a possibility to choose between Aggressive, Moderate and Conservative auto choices. Here are the investment criteria:

Aggressive (LC75) – maximum equity exposure is 75% up to the age of 35

Moderate (LC50) – maximum equity exposure is 50% up to the age of 35

Conservative (LC25) – maximum equity exposure is 25% up to the age of 35

If the participant does not make any selection, then investments are made as per the Moderate plan. Further, any government employee can only choose between Moderate (LC50) asset allocation or Conservative (LC25).

Annuity Service Providers

Upon completion of 60 years, the participant (or Subscriber) has an option to begin Annuity. Below is the list of PFRDA approved insurance companies that offer Annuity:

- HDFC Standard Life Insurance Company Limited

- Star Union Dai-Chi Life Insurance Company Limited

- Life Insurance Corporation of India Limited

- ICICI Prudential Life Insurance Company Limited

- SBI Life Insurance Company Limited

Can a participant change the scheme preferences or investment options?

Yes, the NPS rules allow an option to change preference to a non-government subscriber to design and redesign the portfolio. For instance, a participant can change PFM, as also mentioned above, once in a financial year.

There is an option to switch between Active and Auto choice. In addition, an alternative is available within Active to decide the percentage allocation amongst the available asset classes.

What are the tax advantages and implications in NPS investment?

The National Pension Scheme (NPS) offers several tax advantages, both at the time of investment and withdrawal.

At the time of investment

- An individual who subscribes to NPS can claim a tax benefit of under section 80 CCD (1) within the overall exemption limit of Rs 1.5 Lakhs

- The participant can claim an additional deduction of Rs 50,000 in NPS (Tier I account) under section 80 CCD (1B)

- An additional tax benefit under section 80CCD (2) is available to subscribers under the corporate sector. Employer’s NPS contribution (for an employee) up to 10% of salary (basic plus dearness allowance) is deductible from the taxable income, and there are no limits to this deduction

The above-described tax benefits are only applicable for Tier I account. There are no tax benefits in the Tier II account.

At the time of exit or withdrawal

There are a few options to withdraw, and each has its conditions and tax implications.

Partial withdrawal

A participant can partially withdraw from the NPS Tier I account before attaining the age of 60 years. However, the withdrawal can be only for a specified purpose, capped to 25% of the participant’s contribution. This withdrawal is exempt from tax.

One can make a partial withdrawal under the following conditions, and the amount is exempt from tax:

- A participant must have completed a minimum of three years under the scheme

- The amount of withdrawal cannot exceed 25% of the total contributions made by the participant

- During the tenure of the subscription, a participant can withdraw a maximum of up to three times

- The withdrawal can be for specified reasons, such as:

- Higher education of children

- Marriage of children

- For purchase or construction of a residential house under specified conditions

- Treatment of critical illnesses

In the case of an annuity purchase

The amount invested in Annuity gets exempted from tax. However, the annuity income is subject to income tax.

Lumpsum withdrawal at the age of 60

The participant can make a tax-exempt withdrawal upon attaining 60years of age. The amount is subject to a limit of a maximum of up to 40% of the total corpus.

An example of how you can effectively plan your NPS withdrawal?

Mr Investor has a total corpus of Rs 20 Lakhs at the age of 60years in his NPS account. So he decides to withdraw 40%, i.e. Rs 8 Lakhs, for personal purposes. This withdrawal is exempt from tax, and hence Mr Investor gets the total amount for use.

With the balance, Mr Investor decides to purchase an Annuity. The purchase transaction is again tax exempt. Therefore, he purchases Annuity for Rs 12 Lakhs. Now, Mr Investor starts to earn income from the Annuity. Only that portion of the revenue in subsequent years is subject to income tax.

How can you exit from the NPS or cease to be a subscriber?

Here are the conditions which detail how a participant can exit from an NPS.

On superannuation

Upon reaching the age of 60 (superannuation), a participant can withdraw a maximum of 60% of the corpus funds. The balance of 40% has to be used to purchase Annuity, which provides a steady stream of pension income.

However, there is an exception. If the NPS subscriber corpus is less than Rs 200,000, the participant can opt for 100% as lumpsum withdrawal.

Further, a participant can continue the NPS account beyond 60 years, i.e. up to 70 years. In other words, this essentially postpones the superannuation as well to that age. Contributions made beyond the age of 60 years are also tax-exempt.

Pre-mature exit from the account

A subscriber may choose to exit NPS before superannuation. In other words, before attaining the age of 60 years. However, the exit can only happen after the completion of 10 years as a participant.

In this case, one can withdraw a maximum of 20% of funds as lumpsum. Then, the balance funds must get utilized to purchase an Annuity for regular pension income.

In case of death of a participant

In the case of the participant’s death, the entire corpus gets paid to the legal heir/nominee. However, if desired, the recipient can buy an Annuity instead of a payout.

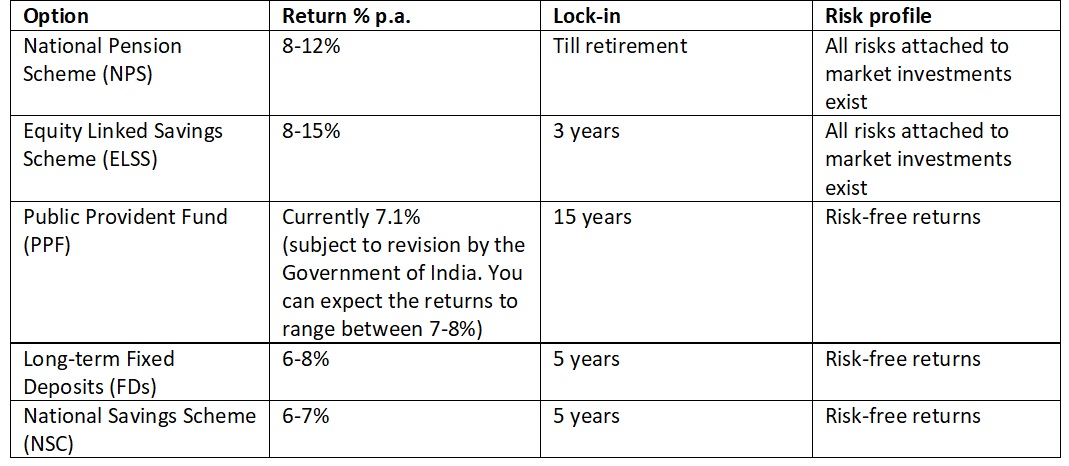

Is NPS better than other tax-saving investments?

There are a few comparable tax-saving options. We must compare to understand which one is the best investment alternative.

NPS has a long term commitment and a long lock-in period. At the same time, NPS earns better returns than PPF, long-term FDs and NSC.

Further, few of the other investment options are more investor-friendly at the time of maturity. For instance, in NPS, there are restrictions on the withdrawal if a participant does not want a tax incidence.

Compared to ELSS, NPS has a more extended lock-in period. Further, ELSS primarily invests in the equity asset class and hence generates higher returns. In other words, if you are an aggressive investor, ELSS could be a better option as equity exposure through NPS may not be sufficient for you.

How can you subscribe to National Pension Scheme (NPS)?

Any individual who wishes to subscribe to NPS can do so online or offline. However, do keep the PAN, Aadhar and bank account details ready at the time of enrolment.

Online enrolment to the NPS

Please visit the website https://enps.nsdl.com/eNPS/NationalPensionSystem.html for enrolment and follow the steps as described below:

- Click on National Pension System

- Select Registration

- Select New Registration

- Fill in the required details

- Upload a scanned copy of a cancelled cheque and the PAN card in *.jpeg/*.jpg/*.png format having file size between 4KB-2MB

- Also upload a scanned and signed photograph in *.jpeg/*.jpg/*.png format having file size between 4KB-5MB

- The website directs you to a payment gateway where you can make payment to your NPS account using the internet banking

- Post this PRAN gets generated within 2-3 days, and you will receive an intimation via email and SMS message

How to authenticate the online enrollment?

After PRAN gets generated, you can authenticate the application in one of the following ways:

- E-sign through Aadhar based OTP

- Send a physical copy of the signed application form to the NSDL office

In the second option, you must print the form, paste a photograph, sign the document and send the documents within 30 days of the date of PRAN generation. In case of a delay, the PRAN gets frozen temporarily.

The prospective participant must send the documents to the below address:

Central Recordkeeping Agency (eNPS), NSDL e-Governance Infrastructure Limited, 1st Floor, Times Tower, Kamala Mills Compound, Senapati Bapat Marg, Lower Parel, Mumbai – 400 013

Offline enrollment to the NPS

You need to fill the PRAN application form. These forms are available with all Point of Presence-Service Providers (POP-SP), or you can download the same from the NSDL website. For a new registration, the correct document is ‘Form CRF – Subscriber Registration Form.’

You can submit a fully filled-in and signed form along with a pasted photograph and KYC documents at the nearest Point of Presence-Service Providers. For quick reference, here is the list of all the POP-SP centres.

How to track the PRAN application for the NPS account?

At the time of submission of the PRAN application, the POP-SP desk provides you with a receipt number. In other words, an acknowledgement of your application. You can track the status of your application by entering the receipt number at the tracking link here.

How to make the first contribution to NPS?

The first contribution to NPS, a minimum of Rs 500, shall be made while registering for the account. After that, you can pay the amount at any POP-SP. For the payment, you must submit an NCIS, i.e., instruction slip, that mentions the details of payment made towards the PRAN account.

A few important websites

Here is a list of a few links that you may find useful

| NSDL website | https://www.nsdl.co.in/ |

| NPS enrollment | https://enps.nsdl.com/eNPS/NationalPensionSystem.html |

| NPS enrollment form | https://npscra.nsdl.co.in/non-goverment-form.php |

| POP-SP centre | https://npscra.nsdl.co.in/pop-sp.php |

| Tracking application status | https://cra-nsdl.com/CRA/pranCardStatusInput.do |

| Fund performance | http://www.npstrust.org.in/return-of-nps-scheme |

| Archive of fund returns | http://www.npstrust.org.in/return-of-nps-scheme-archive |

In conclusion

If the benefits and conditions mentioned above match your investment philosophy, you must consider investing in the National Pension Scheme (NPS). There is no short term in NPS, and the long lock-in period sufficiently clarifies that. The idea is to provide social security and a financially secure life post-retirement.

For the ones who want more equity exposure, better options are available. For example, several mutual funds offer schemes that can fulfil the needs of a diverse set of investors.

In conclusion, properly research and explore multiple options and choose the one that best suits your requirements. In the end, meeting investment objectives and having sufficient corpus is the expected outcome. Do not hesitate to contact your financial advisor for assistance in case of any confusion.

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme caution to avoid possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.