Often, we have heard the saying that Health is Wealth. Taking good care of our health is an important dimension in life. A healthy body is where physical, mental, emotional, and social health is taken care of and that is what helps us lead a happy life. Certainly, this is not a health bulletin, but you will be surprised to know how each of these aspects is integral to the retirement planning process.

Manage your physical and mental well-being

The healthier you are, the happier you live. Studies have proved that individuals with a positive well-being were physically active in their lives and that helps you to remain fit in later years as well. In this era of nuclear families, when you retire you do not want to rely on extended family support, and children, when they grow up, may have to / want to relocate for work and career. Whether you have a family to take care of you when you age, or not, to remain healthy and be able to take care of yourself is always a blessing. Those are the golden days of your life (after your childhood of course). Plan with an open mind so that when the time comes, you are ready to cherish the moments, go places where you could not go before, relax, spend time with loved ones and find peace.

Transition your duties

While this seems to be easy and you might be anxiously waiting for this time to arrive, when the time arrives, it can be challenging. Decide someone to hand over your reigns very carefully and after thorough contemplation. There could be one natural heir (spouse, sibling, son, daughter, etc.) or there could be a need to select someone (internally or externally). The chosen one must have the right mix of business acumen, culture and must share the same values as you. To seclude from work that you have performed for decades is going to be difficult. To curtail the urge to help one in distress is going to substantial. Selecting someone carefully will ease the process of relieving yourself from work.

It is all in the mind

Prepare yourself for your retirement phase and prefer not to enter with a blank canvass. No priorities or plan to spend time may lead you to feel miserable, as this phase of life succeeds an extremely active work life. Make a list of activities you want to do, hobbies you want to pursue, places you want to visit, friends and relatives you want to connect, philanthropy you want to do, community work you want to contribute to, etc. You will look forward to these golden years of life if you know you are going to be socially active and will do what you had wished for a long time.

Once you have tackled non-financial aspects, you can now focus on financial planning for retirement. Retirement planning begins by determining the financial goals with a close eye on the time you have at hand to achieve those. Throughout this process, you must save money and invest it wisely to let the funds grow. Generally, we are talking about decent (to large) sums of money, and hence, understanding the impact of taxes is critical. Any unwarranted tax bill can brutally erase your wealth and hence the retirement plans. Also, a decent understanding of inflation and interest rates regime will be helpful.

Ten steps to plan for your retirement

We list down the most important considerations in the financial planning process for your retirement:

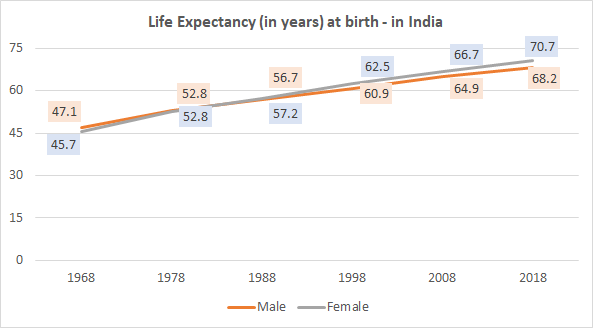

01. Know your time horizon

There are two parts to this – determine the effective earning years available and the number of years for which you should plan for as post-retirement life. Identifying the former can be straightforward in the case of salaried individuals unless the plan is to extend the working years. But in the case of self-employed, you must determine the age until when you can work full steam. The latter is where the challenge lies as no one knows their life expectancy, below chart can be of some help though:

Source: The World Bank Data

02. Risk tolerance

Generally, the higher the number of earning years left, the higher the risk tolerance. Gauging your risk appetite will help you distribute the investible surplus into a suitable asset class

03. Determine living expenses

Split the expected outflow into multiple buckets for clarity in planning – travel, charity, household expenses, gifts, etc. Please remember – to assume that living expenses will significantly reduce after retirement in probabilities is not realistic. Some expenses may reduce (transportation, telecommunication, etc.) while others increase (e.g. charity, travel, social cause costs, etc.). Plan your expenses prudently in each expense category. Do not underestimate as you do not want to be left short of funds, or overestimate as you may witness higher savings pressure immediately

04. Medical expenses

This ideally can be considered a part of living expenses, but given its importance and value, it is important to plan for them separately. As age progresses, health issues and emergencies stand a chance to increase. Mediclaim policies do cover these expenses but certain treatments (e.g. dental care) are not permissible under Mediclaim and routine medical costs cannot be claimed anyway. Therefore, you should plan to cover medical expenses adequately and not let these create a hole in the pocket

05. Identify corpus

Once you have determined the expenses, the future value of current savings should be calculated to help you plan for an appropriate savings that you should do now. Important considerations here are the long-term rate of interest and inflation. This portion of savings should be considered sacred and not disturbed during the investment phase. Another important point is that you must regularly review the progress of your corpus savings and make necessary changes at the right time. Any state or central contributions (provident fund etc.) must be factored as available for corpus in your calculations

06. Plan for uncertainties

Life is unpredictable and can put us in situations that we may not have expected. Such adverse circumstances can create financial turmoil and bring in unwarranted difficulties. You should plan to create a decent-sized corpus to take care of such contingent events without really hindering retirement goals, and this is completely different from the retirement corpus we spoke about in an earlier point

07. Consider only post-tax returns

Often people fail to appropriately account for applicable taxes in the financial planning exercise. Depending upon the income you generate, it may be subject to taxes like securities transaction tax or capital gains tax (short or long term). Your financial planning must account for taxes that you will have to pay exchequer

08. Risk vs. Returns

Your investment decision and returns are relative to the risk you seek. The aim is always to maximize your returns by optimizing risks; not a taking risk at all at an age when you should take the risk (or taking a risk when you should not) can significantly impact the prospects of your portfolio’s performance

09. Real estate

Most often, real estate forms a big chunk of the net worth of an individual. From a financial planning perspective, the house will shelter you, and that is all. Howsoever significant in value, unless there is a plan to liquidate or rent out, a house is often not a source to earn from. Also, real estate transactions are prone to tax implications. Estate ownership is also complicated as it demands maintenance and must be planned adequately

10. Create a will

There is no right time to create a will and there is no real need to wait until the later part of life to create one. As soon as you are clear in your mind, do execute a will to avoid any hassles within the family in future

Read more about the subject of will in my article here – https://decodefinance.in/finance/essentials-of-creating-a-will/

Sale and Leaseback – a possible option

A financial arrangement wherein you sell the home with a pre-aligned understanding to leaseback the same immediately is called Sale and Leaseback. The outcome is twofold, (1) you get immediate cash inflow, and (2) you can continue to live in the same house. Sale and leaseback arrangements provide you immunity from future real estate price fluctuations. The flip side is that you lose from any increase in prices and that you get a huge sum of money at the time of sale. You must have a plan to safely invest the capital and earn from it.

This transaction can also work the reverse way wherein you wanted to buy a house of your choice, and it is available for sale but do not want to go and reside there immediately. You can buy the house and lease it back to existing residents until you are ready to move in.

To conclude

The best retirement plan is to plan for your retirement and not be surprised when you enter that phase of life. To reiterate, those are the golden years of your life and you must take all possible efforts to ensure that turns out to be true. Be ready to sit back, relax, fulfill your dreams, take up a social cause, and spend time with your family and loved ones. Plan well in advance so that your earnings are enough to meet your living expenses (inflation-adjusted) while still preserving the portfolio value. Eventually, if the portfolio outlives your life, it gets transferred to the heir or beneficiaries as per the legal ownership.

——————————————————————————————————–

The author of this article is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity towards the subject of personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The article is based on the author’s knowledge, experience, and understanding of the subject. Any views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under no circumstances the author shall be liable for any views or analysis expressed in this note. Further, the views expressed are not binding on any authority or Court. Readers are advised to consult their financial advisor for advice for their specific case.

Follow our step-by-step retirement planning guide with Us. Connect with a retirement financial advisor for personalized strategies to secure your future.

Thoughtful work. We earn and spent for our dreams but never think of future finance so deeply.