Mutual funds are a popular form of investing in today’s times. Investors get attracted to mutual funds given the flexibility and benefits it offers. Some of the common advantages are:

- Start with a small amount (e.g. Rs 1,000)

- Diversification across asset classes possible irrespective of the investment amount

- Systematic investment plan (SIP) habituates investors to save a fixed amount monthly

- It does not require opening a Demat account

- Buying and selling is quite simple

However, a few still feel investing in mutual funds is a complicated process. And, if you are a beginner, the perceived difficulty is even more. In case you are one of the above, you have landed at the right place. This article will explain all the critical steps to get you started on the investment journey.

Know what is a mutual fund

A mutual fund invests in securities, bonds, money market instruments, and other assets. Mutual fund managers professionally manage these funds, and the attempt is to generate income and appreciate the investment value. We can split mutual funds into three broad categories:

Equity funds

These invest in equity shares of listed companies. Equity funds are considered suitable for investors who have a long-term investment horizon. An equity asset class is ideal for investors who are willing to take moderate risk.

Debt funds

These invest in fixed income securities such as government bills or corporate deposits. Debt funds are less risky, and as a result, offer lower returns. A debt asset class is ideal for investors who wish to take a lower risk and are willing to compromise returns.

Hybrid funds

These invest in a mix of equity shares and fixed income securities. The idea is to maintain the right balance between risk and return. The fund managers operate within a specific ratio of equity and debt investment based on their market assessment.

Gearing up to become an investor

There are a few essential pre-requisites as you begin the investment journey. You must:

- Have an active bank account

- Permanent Account Number (PAN)

- Aadhar number

- Be Know Your Customer (KYC) compliant

Check your KYC status here – https://camskra.com/

If unregistered, you can get KYC registration done either through the agent or through the mutual fund house. A few documents, like address proof, identity proof and passport-sized photographs, will be required to complete the registration process.

Choosing the right fund

More than a dozen asset management companies offer over a thousand mutual fund schemes. A few parameters will help you decide the type of mutual fund. Those are:

- Financial goals (decide investment horizon)

- Risk tolerance (choose between equity, debt and hybrid funds)

- Regular or ad hoc investing (determine the way of investing between SIP or lumpsum)

- Ongoing cash requirements or compounding returns (decide between dividend and growth option)

Read here to understand more about ‘how to choose the right mutual fund.’

How many mutual funds to buy?

Once you have assembled thoughts around these essential aspects, the next question is to understand how many funds to buy. Generally speaking, even by investing in one equity mutual fund, the investment is split into 30-50 stocks spread across sectors. By investing in 3-5 mutual funds, you will achieve significant diversification. Investing in more funds is just splitting the hair too thin, and you will duplicate the underlying equities.

To better understand the concept of portfolio diversification through mutual funds, ‘read here’.

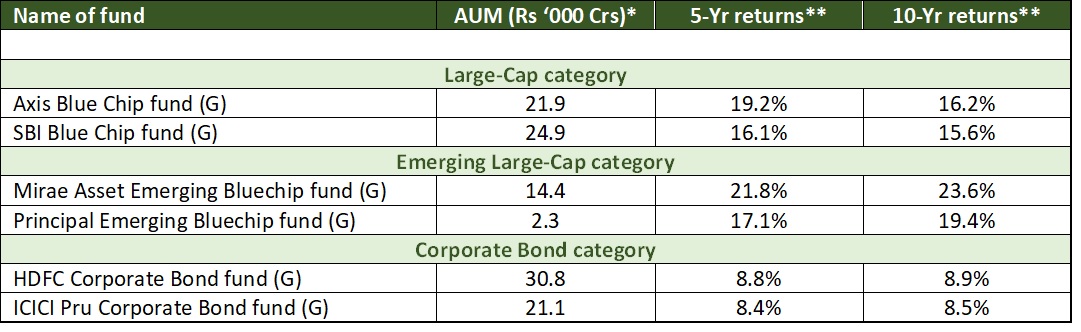

Example of a few popular mutual funds

You should not chase history, but the fund’s past returns provide an important indication. The fund objective and investment rationale will also help you decide if the fund is suitable for your portfolio. For amateur investors, the advice is to start with less risky large-cap equity funds or corporate debt funds. Some examples are listed below:

Buying the mutual fund

After deciding which fund to buy, the next step is to do the actual transaction of purchase. There are two choices here:

Invest directly from a fund house or through a third-party

Both direct and third-party intermediaries are easy to execute.

Direct investment can happen through the mutual-fund house website, online banking services or by visiting the branch office of the asset management company. Few documents will need to be submitted to activate the purchase transaction through a third-party.

A systematic investment plan (SIP) or a lumpsum investment

In the SIP method, a fixed amount gets invested in the selected mutual fund scheme. Usually, the investment frequency is monthly, and acquisition happens on a specified date. A one-time investment occurs in the lumpsum purchase method.

Are you confused between SIP or lumpsum? Read the article ‘SIP or lumpsum’ to help you make the decision.

Selling a mutual fund investment

Professionals manage mutual fund investments, and regular monitoring is not required. I still recommended conducting an in-depth portfolio review at least once a year. Based on the portfolio review, you may decide to sell specific investments to accommodate a significant change in value or adjust for the fund’s underperformance. Alternatively, it would be best to sell funds when you have met the objective for making that investment.

Gains from the sale of a mutual fund may be subject to capital gains tax. Depending on the investment duration, profits will be taxed either as short-term or long-term capital gains tax.

Read my article on ‘How to know when to sell a mutual fund’ to know more on this subject.

—————————————————————–

The author is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity for personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The author has used his knowledge, experience, and understanding of the subject to write this article. Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

Start mutual funds basics for beginners with Us. Learn about investing in mutual funds and discover strategies for beginner mutual fund investments.

Excellent guide for amateur investors.