Most important decisions in the investing journey relate to choosing from dozens of mutual fund schemes, stocks, and fixed income instruments. And the next important question is how to make that investment – the two most commonly exercised options are investing through a systematic investment plan (SIP) or a lumpsum investment.

More about Systematic Investment Plan (SIP)

As the name suggests, SIP means spreading investment into (generally) equal installments over time while lumpsum involves one-time investment; selection of the method has a bearing on investment return, and therefore selecting the right way is vital.

In a systematic investment plan, an investor is expected to contribute regular and equal investments:

- An equal sum of money is invested regularly

- Dates are pre-defined (daily, weekly, monthly, quarterly, etc.)

- Investors with irregular cash-flows must be careful as dates are not flexible

- Usually, the investment happens in the same security/fund

- SIPs work on the concept of cost averaging over a longer period

- Investment in small sums

- Requires a long-term commitment

- It’s a passive way of investing – constant observation is neither required nor recommended

- Imposes discipline on savings and investing

- Benefits of compounding available as interest/dividend get reinvested in growth plans

- Multiple investment options available

- Highly liquid as usually there is no lock-in period (except for tax saving funds, ELSS, etc.)

Lumpsum investment

One time investment, or lumpsum investment, is a one-time investment in a specific security/scheme. There can be multiple tranches of lumpsum investments, but that is based on the availability of investible surplus.

How can lumpsum investment be highly effective

For investors who understand market dynamics and price cycles, to be able to identify a market low (or near low) to invest a lump sum amount can produce high returns and significantly improve portfolio gains. Experienced investors with noteworthy market awareness can benefit from lumpsum investments.

On the other hand, an inopportune investment can result in huge losses. Investors whose lumpsum investments value has significantly eroded hesitate to further introduce fresh money. Due to their lack of confidence in the market or their inability to time the market, they are often not able to recover their losses over a prolonged period.

Let us look through an example

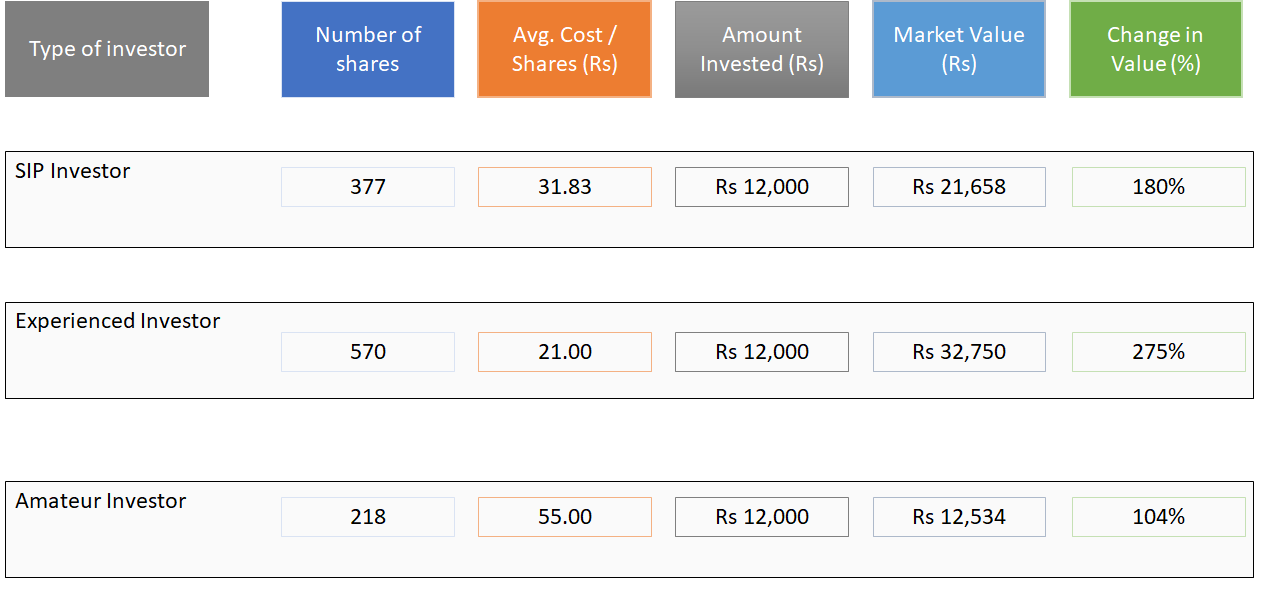

Stock – NCC Limited. The market price as of 24th Dec’20 is Rs 57.45. Prices on the first trading day of each month are given below:

The action taken by each category of investor is as follows:

- A balanced investor follows the SIP route and invests Rs 1,000 on the first trading day of each month

- An experienced investor knows the market and buys at lows (April – May timeframe)

- An amateur investor entered the market in January after experiencing euphoria. The investment turns into a loss and the confidence is low, so the investor does not average the cost. Only now, towards the end of the year and as the market recovers, the market value of the investment is closer to the amount invested

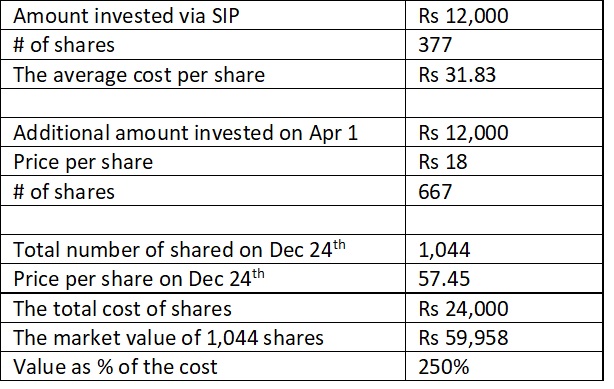

The amateur investor could have taken advantage of the situation if the investor had shown some confidence in the market and stock pick. The person could have invested an equal amount (Rs 12,000) in April – May time when the price per share was Rs 18 to buy additional 667 shares

- The average cost would have reduced to Rs 27.12 per share

- The market value of shares on Dec 24th would have been Rs 50,834, an increase of 212% vs the cost of Rs 24,000 (as against the current 104%)

Though no one can time the market so well and unfortunately, there is no straightforward method to forecast low point (to buy) or high point (to sell). This example was primarily to demonstrate how lumpsum investments can significantly improve returns if done correctly.

The SIP method is better but a hybrid option can be the best

In my personal view investing through SIPs is better for many reasons, such as:

- Helps average the cost of ownership over time (especially during market fluctuations)

- Provides a good option for novice investors who do not have to / want to monitor markets

- Less stressful, specifically in declining markets

- Brings financial discipline through regular savings and investment

- Allows participation even with a small investible amount

Hybrid option is a possibility

You invest through SIP but based on the market understanding, invest lump sums as a mechanism to significantly improve returns.

To conclude

Rule 1 – Investing in any form is better than not investing at all

Rule 2 – Both methods of investing (SIP or lump sum) is good and you can choose either of the two. Factors such as knowledge of the market, income, financial stability, goals, investment horizon, and risk appetite will help you determine the best way forward.

—————————————————————–

The author is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity for personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The author has used his knowledge, experience, and understanding of the subject to write this article. Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

Adds knowledge about subject

Very well explained with precise examples and proper clarity