Many Indians working or settled abroad need to know to know about income tax rules for Indians working abroad. Whether they have any income tax obligation in India or not. To ascertain that, first they must determine their residential status for any given tax year in India. The term residential status must not be confused with an individual’s citizenship in India. An individual may be a citizen of India but may not be a resident from a taxation perspective or non-resident for a particular year. Similarly, a foreign citizen may also become a tax resident of India for a specific year.

Residential status plays an essential role in determining the taxability of income in India. For a tax resident (R) even the global income is subject to tax in India, whereas for non-resident (NR) income that accrues or arises outside India will not be subject to tax in India. Hence it is pertinent to understand residential status as per Indian tax laws.

What is a tax year in India?

- Tax year begins on 1 April and ends 31 March of the following year

- Income earned during the tax year is taxable

- The year you make the income is known as the previous year. It is also called a tax year or the financial year

- Assessment year is the 12 months following the tax year

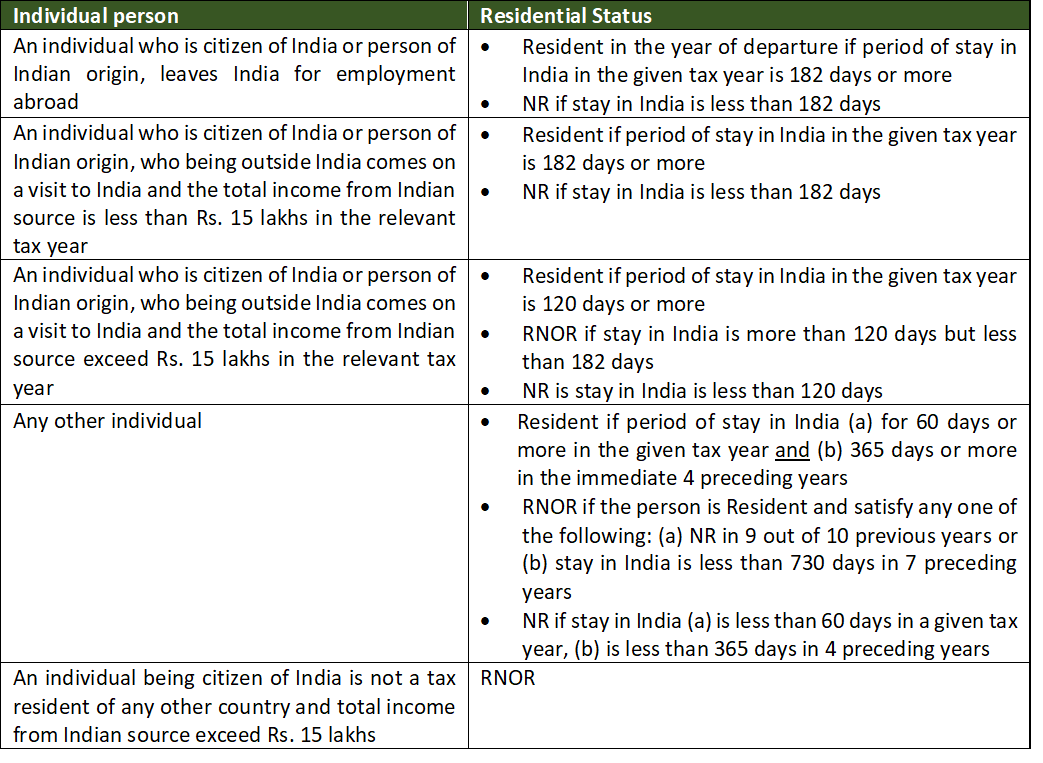

How to determine residential status for an individual?

The Indian income tax law classify a taxable person into three categories, i.e. (1) a resident (2) a resident but not ordinarily resident (RNOR), and (3) non-resident (NR)

2.1 Resident in India

An Individual would be considered as a tax resident of India if s/he satisfies one of the following conditions:

• Stay in India for 182 days or more in a given tax year (i.e. 1 April to 31 March); or

• Stay in India for 60 days or more in the relevant tax year and stay in India for 365 days or more in the immediate four preceding years

The stay of 60 days or more referred above gets replaced by (1) 182 days or (2) 120 days as per below:

(a) An individual who is a citizen of India or person of Indian origin, leaves India for employment abroad or as a member of the crew of an Indian Ship, during any tax year, then 60 days or more will be replaced by 182 days or more. It means individual leaving abroad for employment can become non-resident in the year of departure if the stay in India during the year is less than 182 days

(b) An individual who is a citizen of India or person of Indian origin, who being outside India comes on a visit to India then

a. 60 days or more will be replaced by 120 days or more if the Indian source’s total income exceeds Rs. 15 lakhs in the relevant tax year. It means such Individual can become non-resident if stay in India during the relevant tax year is less than 120 days

b. 60 days or more will be replaced by 182 days or more if his total income from Indian source is less than Rs. 15 lakhs in the relevant tax year. It means such individuals can become non-resident if they stay in India during the relevant tax year is less than 182 days.

2.2 Deemed resident

If an individual being a citizen of India is not a tax resident of any other country, and the total income from Indian source exceeds Rs. 15 lakhs in the relevant tax year, then such Individual will be considered as a tax resident of India irrespective of the period of stay in India.

Income from Indian source means income (a) which is received in India or accrues or arises in India, (b) which is deemed to be accepted in India or deemed to accrue or arise in India or (c) which is derived from a business controlled in India or profession set up in India.

2.3 Resident but not ordinarily resident (RNOR)

Once an individual qualifies as a resident, s/he needs to determine whether the resident is resident but not ordinarily resident (RNOR). A resident Individual is said to be RNOR in India in any tax year if (a) s/he has been a non-resident in India in 9 out of 10 previous tax years or (b) s/he stays in India 729 days or less in 7 immediately preceding years.

Also, a resident individual is a citizen of India or Indian origin having total income from Indian source exceeding Rs. 15 lakhs during the given tax year, becomes RNOR if the stay in India during the relevant year is more than 120 days but less than 182 days. Also, an Individual being resident of India by virtue of being a citizen of India having Indian sourced income exceeding Rs. 15 lakhs in a given tax year and not a tax resident of any other country, will also be considered RNOR.

2.4 Non-resident (NR)

If a person does not qualify as a resident, then s/he is an NR.

The below table summarizes the above-stated details:

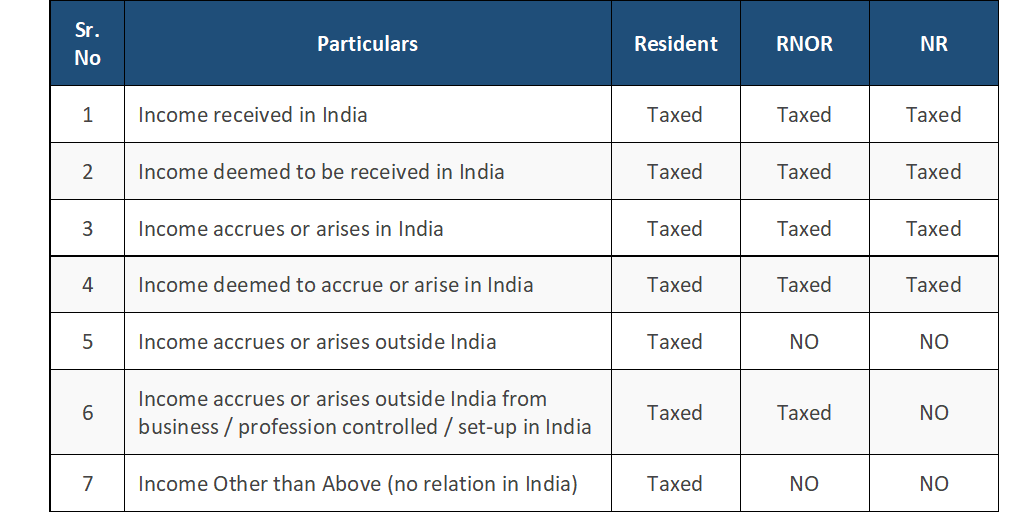

Whether income earned abroad is taxable in India?

Taxability of any income in India depends upon the residential status of the Individual. For a tax resident, global income is subject to tax in India, whereas, for NR, income that accrues or arises or deemed to accrue or arise in India is subject to tax in India.

Illustrative list of incomes which deemed to have accrued or arisen in India:

• If Mr A transfer his residential property situated in Mumbai then capital gain arising on transfer of such capital asset is deemed to accrue in India.

• Income from a business connection in India.

• Dividend paid by an Indian company.

• Income from any property, asset or other sources of income located in India.

• Interest income if such interest is payable for the debts incurred or moneys borrowed and used for business or profession carried on in India.

Income taxability summarized here:

From the above, the following situation emerges:

- Once a person qualifies as a tax resident of India then global income is subject to tax in India, including income from foreign sources

- Income from Indian sources will be subject to tax in India irrespective of residential status. Meaning even NR will have to pay tax in India on Indian sourced income. The only exception is income that accrues or arises outside India from India’s business/profession setup. No tax from income from business/profession set up in India in the hands of NR

- No tax on the income from foreign source in India in the hands of RNOR and NR

How to avoid double taxation?

In the case of NR, income from an Indian source will be subject to tax in India. Further, such income might also be subject to tax in the country of residence of such Individual. So, the same income is taxed twice, in the country of residence and source. However, India has entered into Double Tax Avoidance Agreement (DTAA) with many countries, which avoids double taxation. The relief under DTAA could be either in the form of exemption, meaning such income will be taxed only in one jurisdiction, or in the form of the tax credit, meaning the country of residence will provide appropriate credit for the taxes paid in source country on the same income.

Whether NR is required to file an income tax return in India?

If NR has earned any income from Indian source exceeding the basic exemption limit (which at present is Rs. 2,50,000) in a tax year, then s/he is under an obligation to file his tax return in India. NR also needs to file an income tax return if s/he wants to claim a refund of excess tax withheld or if s/he wants to declare losses incurred to benefit from carrying forward and set off against eligible income in the subsequent year.

The implication of extended stay due to COVID-19 on residential status in India?

Due to lockdown and suspension of international flights due to COVID-19, many people must prolong their stay in India. Considering this situation, the CBDT vide circular no. 11 dated 8 May 2020 announced some relief to avoid genuine hardship due to COVID-19 such that such period of forceful stay in India will not be counted to determine residential status.

As per the circular, there are some specific situations for:

- People who came to India for a visit before 22 March 2020

- Ones who got quarantined in India on or before 1 March 2020

- Those who departed on evacuation flight on or before 31 March 2020

- Or people who were not able to leave India on or before 31 March 2020

In such situation, the period of stay from (a) the date of quarantine or 22 March 2020 to (b) the date of departure on evacuation flight or 31 March 2020, as the case may be, will not be counted for determining the residential status. The above relief is relevant only for the year 2019-20. However similar relief is expected for the year 2020-21 as lockdown continued during 2020-21.

—————————————————————–

The author of this article is Kiran J Nisar, a chartered accountant, tax professional and a registered valuer. Kiran has over 25 years of rich work experience handling tax matters, including providing consultancy services as a business advisor. Currently, Kiran provides consultancy through his firm Kiran Nisar & Co. Reach out to him on his email at kiran_nisar@hotmail.com.

Publisher of the article is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity for personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The author has used his knowledge, experience, and understanding of the subject to write this article. Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.