To accumulate Rs 1 crore in 10 years is a significant milestone for any investor. In other words, to be able to collect such a massive corpus is an outstanding achievement. However, although substantial, the target is achievable through consistent investing and firmly believing in your investment decisions.

There are two options to begin the journey to accumulate Rs 1 crore – a lumpsum investment or regular investment (through a systematic investment plan). While both these options are plausible, I will base my calculations on making monthly equated investments i.e. through a systematic investment plan (SIP). For the benefit of our readers, we have evaluated whether lumpsum or SIP is a better way to invest. However, we firmly believe SIP is a better investment method and therefore, the article uses SIP methodology for calculations.

So, how much should you save every month?

You can accumulate Rs 1 crore by investing Rs 36,500 per month for 10 years (i.e. in 120 months). The calculations assume dividend/interest reinvestment and a 15% annualized rate of return. Assuming a 10% annualized rate of return, the investment per month should be Rs 49,000.

| Monthly amount | Annualized return | Principal invested |

| Rs 36,500 | 15% p.a. | Rs 44 Lacs |

| Rs 49,000 | 10% p.a. | Rs 59 Lacs |

Alternatively, you can choose to increase the per-month investment gradually in anticipation of higher income levels as you progress. Here we assume an increase in the monthly investment amount by 10% each year. In that scenario, you can start with a lower amount as per below:

| Monthly amount | Annualized return | Principal invested |

| Rs 26,000 | 15% p.a. | Rs 49 Lacs |

| Rs 33,500 | 10% p.a. | Rs 63 Lacs |

In the 10th year, your monthly investment would have increased to Rs 60,500 and Rs 78,500 at 15% and 10% returns, respectively.

We have rounded off investment amounts for convenience. Also, we have not factored in gains (upon maturity) that may be subject to capital gain taxes.

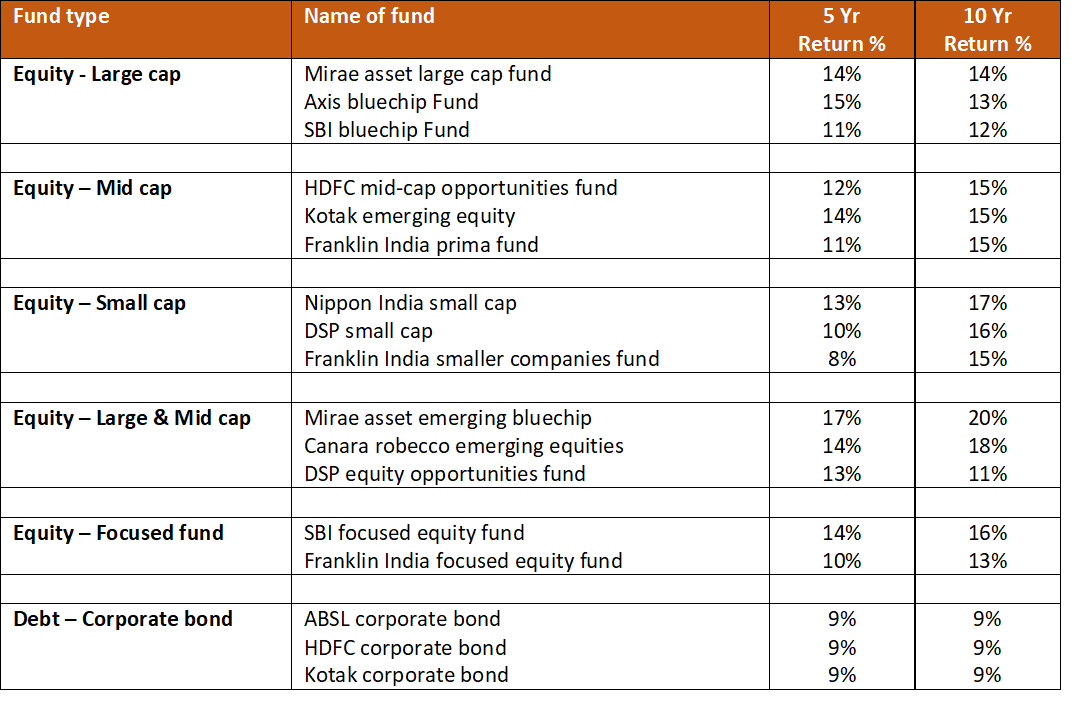

Illustration of historical mutual fund performance

As you read, one obvious question strikes you – is it practical to achieve this level of returns? And, the answer is yes.

We have listed down the historical returns of some of the well-performing mutual fund schemes. And, these funds have achieved returns in the range of 10-15% or even more. Though past returns do not guarantee future performance, it does provide an indication.

Below criteria’s have been used to filter the funds and the list is not exclusive:

- Only select top-performing funds under each category listed here

- We have considered funds with over Rs 5,000 crore of assets under management

- Funds that have been in existence for at least 10 years considered

As you can see and based on the historical performance, achieving a 10-15% return per annum does not seem unreasonable. Of course, profits can be even higher with higher risk, but we do not recommend that. Therefore, we have not factored any unreasonable returns in our calculations.

What can help or deter you from achieving this target:

What will help:

- Investments perform better than expected and achieve higher returns than considered above

- You have the understanding to identify market dips to invest further. In other words, you buy on dips to lower the average cost of ownership

- Despite the risk, you choose to invest in riskier funds, and they earn higher returns

What can deter:

- Long term bear phase in the market may lead to continued underperformance

- Higher than expected capital gain taxes upon maturity

- Disruption or discontinuation during this investment tenure

Here are a few more guiding notes:

Apart from what we have described above, here are a few more guiding principles.

- Do not keep idle money in bank savings account for a long time

- Choose the right mix of risk in your asset portfolio; there is no merit in taking less risk as that diminishes the portfolio performance. Similarly, it would be best if you did not take more risks seeking higher returns

- Always optimize tax expenses

- Buy health policy and term insurance. However, wisely plan the insurance costs and only include beneficial riders

- IPOs of strong companies can offer listing as well as long-term capital appreciation. This additional investment can often be a good source of capital appreciation

- Keep your long and short term investment objectives distinct. Mixing the two will lead you to take financially incorrect decisions

In conclusion

Wealth creation is a matter of consistency and patience. There will be difficult market conditions, and you must act prudently. Do remember mutual funds, shares, fixed income bonds are all subject to market risks. Selecting the right mix of funds and regularly investing in those will help you achieve financial goals. Also, evaluate your portfolio performance at least once a year and make necessary adjustments.

Investment is always a matter of prudence and is long term in nature. Do seek guidance from your financial advisor in case of any doubts.

Happy Investing!

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme caution to avoid possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

Helpful to make your dream true.

Very insightful and easy to understand the formula of wealth accumulation

I was eagerly awaiting for this blog time.

Thank-You this would be really helpful to reach 1 crore in line of 10 Years.

Very helpful and informative