You work hard to ensure the needs of your loved ones are fulfilled and they get to experience the best in life. The family deserves it. Term insurance, the purest form of life cover, is the most conventional form of insurance. Term insurance benefit – financial independence of your family is not compromised in your absence. Return of term insurance involves payout of the sum assured as a lump sum in case of death of the insured. People seldom get confused about the utility of life insurance and that is what we want to elucidate here.

- Who should buy term insurance?

- What is the right amount?

- What if one outlives the insurance tenure?

- The right age to buy term insurance?

- Will I get the sum assured?

Do you have a family – dependent parents, spouse, dependent children, or siblings? If the answer is yes, then it is essential to buy a term insurance policy. In case of an untoward incident of death, the arrival of insurance funds (i.e. sum assured) can be a real blessing. These funds can:

- Help maintain the lifestyle of surviving family members

- Pay-off recent medical bills

- Meet short-term family goals (child education, marriage in family, etc.)

- Protect erosion of family wealth

- Pay any existing loans

Buying term insurance is simple

Yes, its very simple to buy term insurance. You can buy it online from any insurer’s website, offline by a visit to the insurer’s office, or through an authorized agent or third-party websites. The insurance premium is generally fixed and is paid over the length of the policy term. Premium also qualifies for tax benefits under section 80C of the Income Tax Act.

Return on investment in case of a term insurance

Return in the form of lump sum payment is expected in case of death of the policyholder, which essentially means – if the policyholder outlives the policy tenure, there will not be a return. The idea here is not to earn, instead, the objective is to provide financial security to the family. Consider this as an umbrella that saves your family from an untimely rain (demise of the policyholder).

How much term insurance should you buy?

There is no scientific term insurance calculator to determine the term insurance amount, but it is suggested that the sum assured should be in the range of 5-10x the annual income. Alternatively, multiply your annual income with the balance numbers of earning years left to arrive at the sum assured.

Example 1 –

Current age 25Yrs. The income of Rs5Lacs p.a. Earning age until 60Yrs

| (a) | (b) | (c) |

| 5X Income | 10X Income | Income X Balance earning years |

| Rs25 Lacs | Rs50 Lacs | 5 X 35 = Rs 1.75 Crores |

>> Recommended term insurance value in the range of Rs 50 Lacs – 1.0 Crore

Example 2 –

Current age 55Yrs. The income of Rs40Lacs p.a. Earning age 60Yrs

| (a) | (b) | (c) |

| 5X Income | 10X Income | Income X Balance earning years |

| Rs 2 Crores | Rs 4 Crores | 40 X 5 = Rs 2 Crores |

>> Recommended term insurance value in the range of Rs 2.5 – 3.5 Crores

Example 3 –

Alternative way is to consider the outlays to determine the principal required to earn equivalent interest through bank fixed deposits.

- Cost of living based on city of residence

- Big-ticket expenses like child education/marriage

- Existing debts and installments

- Number of dependents and their age

- The medical condition of dependents

Consider a bank interest rate scenario of 5.5% p.a. In continuation from the above, below is how we can determine the sum assured.

Example 1 – annual expenses of approx. Rs 4.5 Lacs. The sum required is Rs 82 Lacs. (4.5 Lacs divided by 5.5%)

Example 2 – annual expenses of approx. Rs 20 Lacs. The sum required is Rs 3.6 Crores

Remember to account for all state & central government personal taxes. Those have not been factored in the above calculations. For instance, if you are liable to pay 10% of your annual interest income in tax, then in example 1, the sum assured should be Rs91 Lacs.

Insurance premium and riders

Premium is based on the age and health of ‘to be’ insured at the time of the policy issuance. The premium is generally low if you subscribe to a policy at a young age. If you have not yet bought the policy, purchase it now – just that the premium will slightly more and, costly premium due to late entry age is a disadvantage of term insurance.

Insurance companies do offer benefits (also called riders) that are worth considering – but remember any additional benefit comes at an additional cost. Some of the riders are:

- Life cover extended up to 85 years of age

- Continued monthly payments, over and above lumpsum settlement at the time of death of insured

- Waiver of premium in case of permanent disability of insured, but the policy continues

- The additional sum assured in case of death due to an accident

- Insured gets an assured sum in case of getting diagnosed with a critical or terminal illness

Insurers also offer joint term insurance policies. This works on the principle of first death – if any one of the two insured persons die, the surviving policyholder receives the lump sum pay-out of the sum assured.

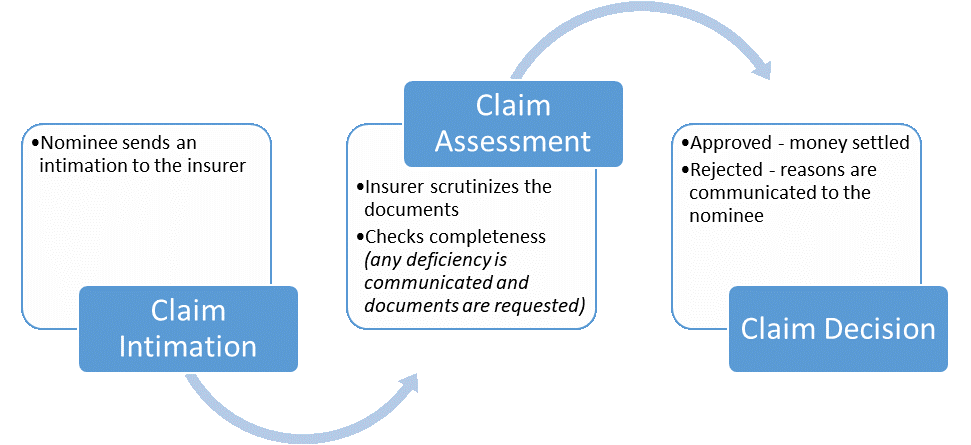

Documentation for claim processing

To complete the term insurance claim process, these documents are required:

- Duly filled in claim forms as provided by the insurer

- Original policy documents

- Post-mortem / FIR / viscera report (as may be applicable)

- Certificate from physician/hospital showing the cause of death and other medical records

- Age and identity proofs of deceased and nominee

- Any other documents as may be specifically required by the insurer

Claim process is simple and settlement ratio is high

Usually, the claim process is straight forward:

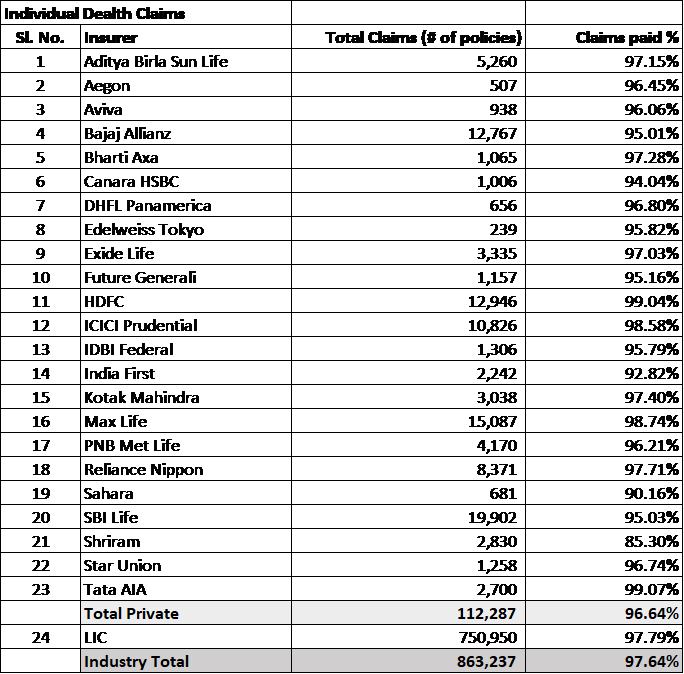

The settlement ratio in case of death claims is usually high. Still, over two out of a hundred claims are not processed in favor of the insured. The below table illustrates the number of claims in the last year and the settlement ratio across insurers:

Source: IRDAI Annual Report 2018-2019

To conclude

A term insurance policy is not an investment plan, never buy term insurance with an expectation of a return. Receipt of sum assured in case of an untoward incident should relieve you of worries about the financial security of your family. Think prudent and be futuristic as you decide the term insurance amount and choose the insurance company.

————————————————–

The author of this article is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity towards the subject of personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer: The article is based on the author’s knowledge, experience, and understanding of the subject. Any views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under no circumstances the author shall be liable for any views or analysis expressed in this note. Further, the views expressed are not binding on any authority or Court. Readers are advised to consult their financial advisor for advice for their specific case.

People are very casual about term insurance. Contents of article will help people to understand the hard need of term insurance.

Thank you.

very nice and detail explanation.

very useful to all

Very lucid and comprehensive note. Equally helpful for finance and non finance background people

The given information is very useful.

Citizens should always look up to major things like insurance.

Wonderful write up Sagar, an important concept explained in a simplified and effective manner. Thanks for sharing your good insights.

To the point.

After unprecedented times such as now, more and more people need to get educated about Term plan and this article will help a lot in it.

This is unfortunate that still many people feel that insurance is waste of money however infact it’s a futuristic approach to safe family from unexpected incident with main earning member.

Explanation given in the article is good enough to understand importance of term insurance.

I liked it, would request you to please also publish article on importance of health insurance so that we can forward to our friend circle.

Thanks !!

Hi Sagar, very nice and well explained the concept in your article.

Term insurance or life insurance is a must in today’s world of growing uncertainty and inflation.

If there are dependent family members it is must

I heard few people saying that my partner is earning sufficient, so tomorrow it doesn’t matter whether I am there or not, however, I still feel there is some value attached to each one’s life, so let them donate the money of the death claim if they don’t really need, but take life insurance, agree the presence of the individual cannot be compensated by money, but some support family will certainly get by the claim money.

Term Insurance is a must for every individual on whom his or her family is dependent. Excellent article explaining the entire process and checks for taking it. Great one Sagar !

Precisely explained article about the term insurance.

Article very nicely explains the need for term insurance and how to decide the amount of insurance. Have learned a lot from this article and will implement it.

Extremely informative with nice examples to understand each point. It’s time people differentiate between investment and insurance. Term insurance should be #1 on the list and company with better than industry claim settlement ratios should be the choice

Very nicely explained..

Precise and to the point.Very helpful and examples made the writeup more clear and easy to understand..

You could include brief on major terms that should consider like do’s and don’ts while going for a Term Insurance first time..

For someone who’s just starting off with their career, this one’s an explicit read! It’s quite simplified and absolutely understandable!

A great reckoner for the uninitiated. Lucid writing style and easy to follow examples. And comprehensive. Great work, Sagar

Thank you Fareed !