How to make a financial plan by yourself? Do you resonate with these words? Financial planning may appear very familiar for some and a distant thought for others. For the latter, to make a financial plan by self is beyond the stretch of the imagination. Although financial planning may sound unfamiliar still, we all use those techniques in our lives each day. The idea here is to give a structure to thoughts and follow the proper steps. If you follow the process religiously, you can build a reasonably robust financial plan by yourself.

Financial planning is a process to estimate the corpus requirements and identify means to achieve the same. It is a step-by-step progression. The financial plan helps you manage income and expenses and acts as a guide in your financial journey. The steps cover every aspect that can economically affect you that you can predict. Various elements like debt and investments strategy, retirement plan, contingency and insurance requirements, and tax optimization get covered. Read about the importance of financial planning in India here.

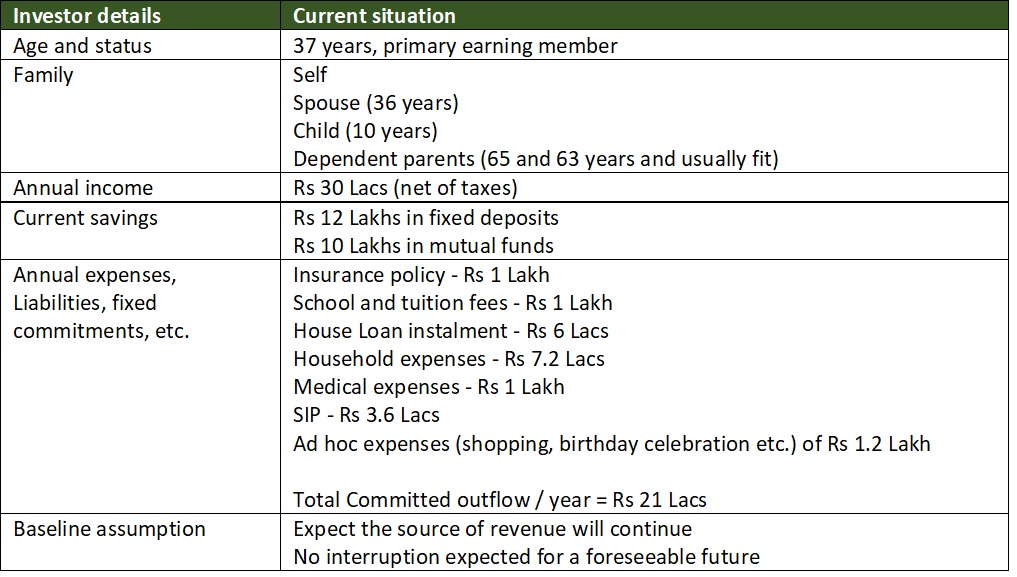

Using a real-life example, let us dive into a model and understand how to make a financial plan in detail.

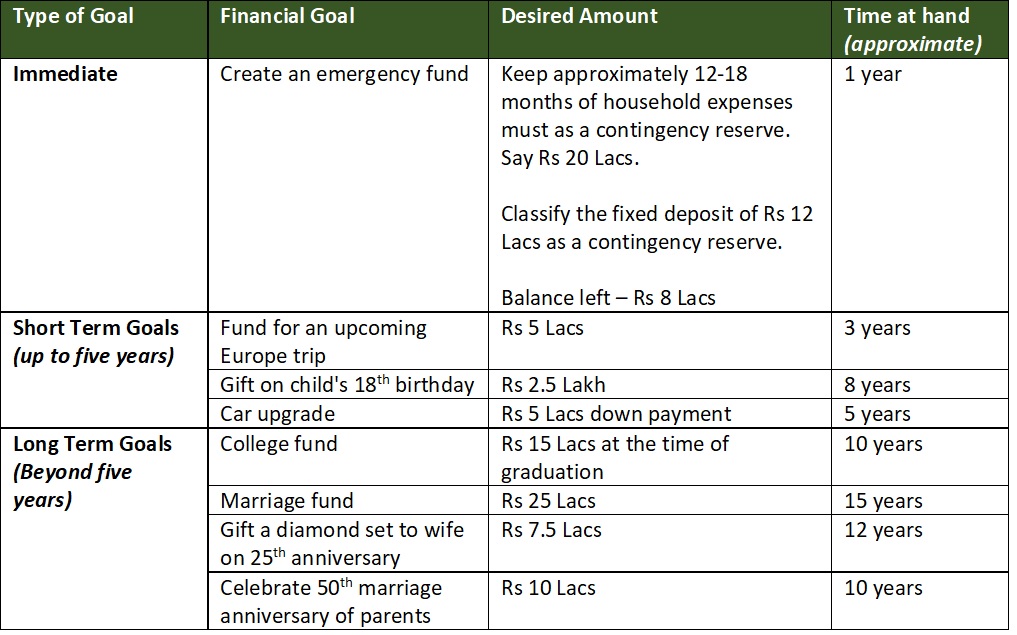

Establish the financial goals (Step 1)

The routine household expenses will continue as it is. The objective here is to list down the goals that need special attention and target savings.

The first step is to list down the saving needs in a framework:

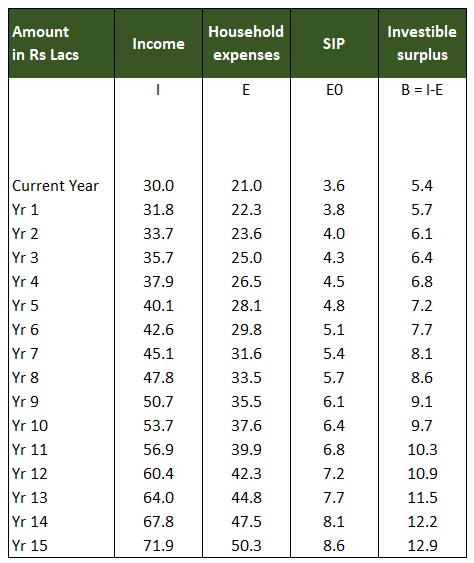

Make an investment plan to meet those objectives (Step 2)

Once you have established the essential financial goals, the next step is to make an investment plan to help you achieve those objectives.

There are a certain assumptions to make in this process:

- Income will continue and increase at 6% per year

- Household expenses will increase by 4%. Although the inflation rate is more (5-7%), a few outflows like insurance premium etc., do not grow at the same rate. Hence we should consider a hybrid rate

- SIP of Rs 3.6 Lacs will continue and increase at the rate of growth in income

- Assume a net annualized rate of return of 8% on investments

With the above assumptions, let us understand how you can draft the investment plan.

Determine the investible surplus, i.e. total inflows after deducting household expenses and committed outflows (like SIP in this case). There is an option to tag the SIP to one of the targets. Alternatively, you can keep it separate, as we have done in this example.

After determining the surplus available for investment, the next step is to make an allocation plan.

Split the goals

Begin by splitting the goals into immediate need, short term and long term. The bifurcation of goals into duration helps you gauge the urgency and attention each one requires.

As you can imagine, one essential dimension is to attach priority to each goal.

For example, the objectives with the highest focus start first. You will notice in the table above that investment for some lines have started immediately. In contrast, others begin in the subsequent years.

Be pragmatic to modify goals as necessary

There is always an option to eliminate a goal if found not reasonable. However, some of the goals will be time-sensitive, and the investment plan must consider the same.

Remember –

Financial resources are always limited, and you must plan for the best possible utilization of those.

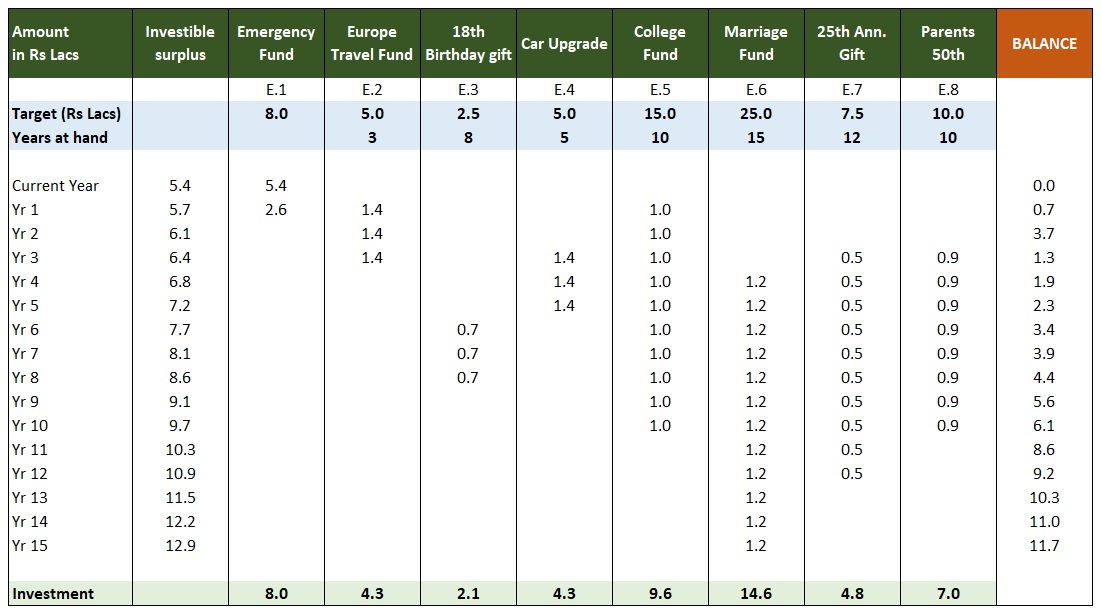

A few basic assumptions to better understand the table:

- Emergency fund is essential and is assigned the highest priority

- Goal-based investment plan starts at different points in time based on importance and years at the hand

- The principal value of investment considers an average rate of return of 8% p.a. on the investments

- For instance, Rs 1.4 lacs invested per year at 8% p.a. return will become Rs 5 Lacs at the end of 3 years which is the Target for European travel

- Principal sum of Rs 4.5 Lacs to achieve Target of Rs 5 Lacs

- A plan to invest the balance funds not included here – these funds can be utilized or invested as that time arrives

Individualized situations excluded from the calculations

Circumstances are highly personalized. Therefore, any such personal situation has been excluded from the example above. You would need to alter the investment plan to best suit your requirements:

- Inherited assets (e.g. house, antiques, precious stones, ornaments etc.)

- Unforeseen expenses (e.g. medical, settling a liability)

- Interruption in income

- Windfall gains

- Etc.

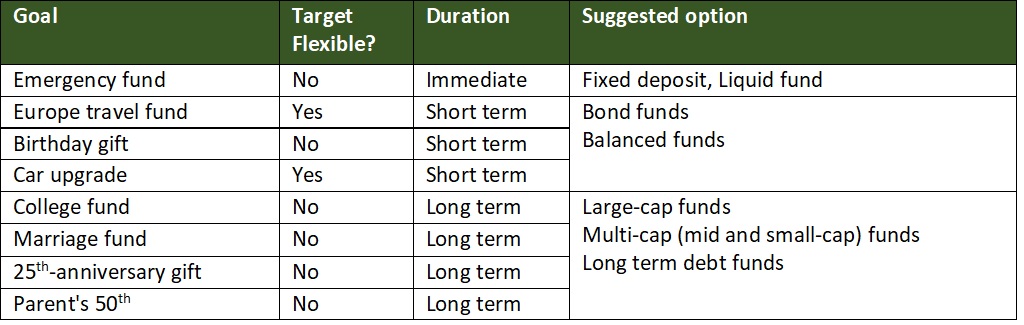

Identify investment options (Step 3)

The first two steps talk about how to determine the financial objectives and their respective timelines. That is half the battle. The next crucial step is to make an investment strategy that helps you direct savings into investments. After, to chase those financial targets is the ultimate objective.

Do read about how to select mutual funds here based on your risk appetite and investment horizon. Below is an example of investment options you can consider.

Options are plenty but selection is critical

The above options are only indicative, and you must evaluate multiple options. You must base the fund selection on parameters like time duration, goal flexibility and risk appetite.

For instance, in the above example, the marriage fund target is not considered as flexible. However, because it is long term in nature, you may take a moderate risk. Consider investing a portion of the amount in mid-cap or small-cap mutual funds.

The value of the investment fluctuates with market movements. Therefore, it is necessary to assess the portfolio performance and progress towards the targets. A diligently crafted plan may not require significant changes. Still, regular assessment of fund performance, at least once a year, is highly recommended.

Why is financial planning important in India?

In India, financial knowledge is limited, and there is a need to improve awareness. Growing income levels make it even more important to educate people on aspects of financial planning.

Further, rising life expectancy and technological advancements in medical sciences demand better insurance coverage and a larger retirement corpus. To live long happily requires you to plan for enough means to make ends meet.

The evolution of the nuclear family structure expects financial readiness at every unit of the family. Earlier, the primary member of the house took the burden of managing family finances. The decentralization makes it critical for a more comprehensive understanding of financial planning.

Social security is not up to the mark in India. There are systems and procedures, government support is also available, but that is usually not enough.

All these aspects direct you to a clear point of consideration – be financially ready and plan for your future.

Build a financial plan by yourself or seek expert help, but start now!

Financial planning is like navigation when you drive. If you know the destination, steering becomes easy. The challenge arises when you are not aware of the goal. The process can is slightly elaborate. But follow the process as mentioned above, and the outcome will be rewarding. You do not have to be visionary but certainly need some financial acumen.

Still feel financial planning is not your cup of tea; seek guidance from a financial advisor. A short-lived financial plan is of no value.

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme care and caution to avoid any possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

Learn What is Personal Financial Planning with us. A Guide to Financial Planning for Beginners, covering Basic Personal Finance Strategies.

Great work Sagar such a descriptive knowledge sharing and meticulously covered all the aspects. This would be a great help for a layman like me

Thanks for sharing!