What is the right age to begin investing? The answer is, one should start investing as soon as the person is lawfully allowed to invest. In this article, we will elucidate upon the power of compounding and benefits of early investing.

Early-stage investing helps in many ways, and one of the most significant benefits is the power of compounding.

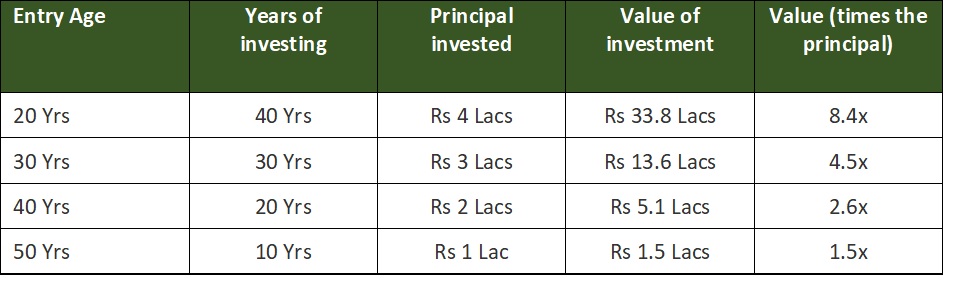

The power of compounding is a straightforward concept. Suppose, you invest Rs 10,000 once a year, at a 9% rate of return. The one who started investing at the age of 20 Yrs gets significantly higher returns compared to the ones who began later. And that is the power of compounding returns.

The table below demonstrates the market value of the investments at the age of 60, but started at different points of time:

As you can see, the benefit of compounding is more than just the factor of the number of years of investing. More about this later in the article.

Do read about – “How to accumulate Rs 1 Crore in 10 years“ here.

Top-seven advantages of early investing

Here are the most important takeaways from the above example that explains about the benefits of early investing.

01. The power of compounding is multifold in early-stage investing

The advantage of early investing is the number of times your investment return compounds (i.e. you earn a return on the return). Out of the total 40 years of the entire investment planning in our example, starting at 20years or 30years means a gap of only 10years. That essentially means 25% of the overall investment span. However, the gap in returns, 8.4x when started at 20 years vs 4.5x when started at 30 years, is significantly more.

02. More time to recover when you begin early

If you incur a loss or face a decline in the value of investments, you will get more time to recover when you begin early. In the above example, the investor who started at the age of 20years has more time to manage the investments.

03. More savings in the early phase of life

To start to save when you are young is possible. The income can be low as you would have just begun the career. Still, at the same time, liabilities and requirements are also limited.

04. Rhythm to save sets-in early

Many people are not able to set a saving rhythm, even when they wish to. That may be because outflows are more than inflows or just that the expenses are not well planned. When you begin investing early in life, mental mathematics works to save first and helps you fulfil the investment objectives.

05. Be in a position to help others

Often you come across situations where either your friend, family member or a close colleague needs money. Your investment or spare money will position you as someone who can help others in the time of need. A sense of satisfaction will prevail when the near and dear ones will remember you for the financial help you once offered.

06. Better risk-taking

More-risk earns a better reward. Usually, young investors have a higher risk-taking capacity and are more likely to achieve a higher risk-adjusted return. Hence, there is a high probability of making a handsome return when you start investing early.

07. Support your early retirement plans

Early investing will help you to save the retirement corpus sooner in life. The amount of money is dependent on several parameters, which are individualized. Irrespective of the goal you want to achieve, an early start will immensely benefit the process.

Do read about ‘How much money you require to retire’.

The meaning and the power of compounding

In the financial world, compounding happens when income on your investment starts to earn income.

The compounding occurs through the reinvestment of income. The process creates a chain reaction, wherein income gets reinvested, earns additional income until the investment exists.

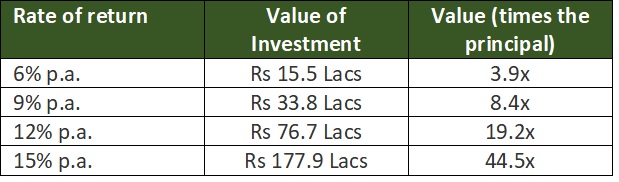

Return rate plays a vital role in compounding – the table below is in continuation of the above example where a person invests Rs 10,000 per year for 40 years.

The impact of change in the rate of interest has a disproportionate impact on the market value. For instance, by doubling the return rate from 6% to 12%, the value increases from 3.9x the principle value to 19.2x.

Time duration is another critical parameter, which we have discussed earlier in the article.

Save before you spend

Usually, the Indian households are good at following a regular savings discipline. Being an early investor forces you to save before you spend. A dedicated amount gets earmarked as an investment. It gets removed from the bank account, leaving you to manage expenses from the balance. And, that is the right way to manage the costs. Savings is always a percentage of income, and not residual of income after meeting expenses.

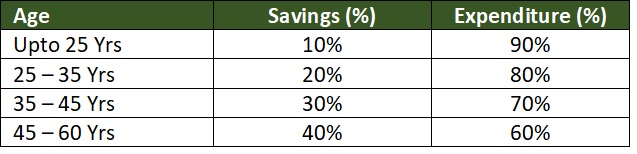

The below table indicates the suggested Savings-to-Income (S2I) ratio for different age brackets.

You may read more about this in my article “Thumb rules of financial planning.“

Investing through SIP can be increased with time as income grows. Say, in the case of a salaried person, you may decide to dedicate a third of your increment each year into savings. And every incremental amount saved will compound over time.

Read about “SIP or lumpsum investing“ in my earlier article.

Bottom line – there are tangible benefits of early investing

By starting early, you get the most use of compounding returns. Other apparent advantages are –

- Develop the discipline of investing

- Exercising patience through market ups and downs

- Long-duration helps lower the average cost of ownership

- Ability to better understand the external factors

- Enough time to plan tax impact

- Flexibility of take chances and learn from failures and successes

There are many benefits of early investing, and the sooner you start to invest, the better it is.

Happy investing!

The author is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity for personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The author has used his knowledge, experience, and understanding of the subject to write this article. Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial planning advisor for assistance in their specific case.

Discover the power of compounding money with us. Learn the benefits of early investing and explore effective compound investment plans for wealth growth