An investment strategy aims to meet financial goals keeping in mind risk appetite and individual preferences. Creating an investment purpose serves as a guide to developing an investment plan – here are thumb rules to make an investment plan that help you begin and construct the investment framework:

- Define financial goals, i.e. state your investment objective (Box Framework):

- Split into short term (e.g. to purchase a new car next year) and longer-term (e.g. to pay for child college fees after eight years)

- Split into a non-compromising goal (e.g. marriage of your children) vs flexible purpose (e.g. travel)

- Determine a principal savings amount, not tagged to any goal

- Identify the available asset classes – Equities, Bonds, Property, Gold, Cash, Insurance, Investment in business, etc.

- Determine risk tolerance

- Note down investment constraints (e.g. choices, liquidity preference, etc.)

- Understand tax implications (transactions tax, capital gains taxes)

Portfolio rebalancing

Once you have fixed the asset portfolio and allocation mix, there may be a need to rebalance the portfolio to stick to your defined allocation proportion. For instance, you have Rs100 and want 75%:25% split into equity and cash. One year later, equities grew by 20%, and liquid money was as is. Now the equity value is Rs90, and cash is Rs25. The revised split is 78%:22%; therefore, a need to rebalance the portfolio. It would help if you had a strategy to rebalance your portfolio:

- Value-based – significant increase or decrease in value of an asset will pose a need to rebalance

- Time-based – Annual Performance Review (APR) is a popular concept. Assess rebalancing needs at pre-determined time-frequency

- No rebalance – you may decide not to rebalance the portfolio, but you must understand its merits and demerits

A few tumb rules to make an investment plan are always useful. Whether you are naïve in your investment journey or are an avid investor, these rules will help you channelize your investments in the right direction. These are general guidelines, and you must seek expert advice at a later stage.

THE first rule of thumb – Create an emergency fund

Was there fear of the loss of income during this pandemic? Create an Emergency corpus even before you begin your long-term investment journey. Any setback in your earning capability, temporarily due to unemployment or prolonged, will challenge you to keep it going and meet household expenses. In another situation, a medical emergency may create immediate liquidity requirements while claim the settlement happens subsequently. Commitment towards EMIs is also fixed and will not change with a change in your financial conditions.

An emergency fund aims to let you meet your needs and is outside the scope of your financial goals. As a rule of thumb, living expenses of 12-18 months should be the size of your emergency fund. To create an emergency corpus is Step Zero.

Determine how much to save

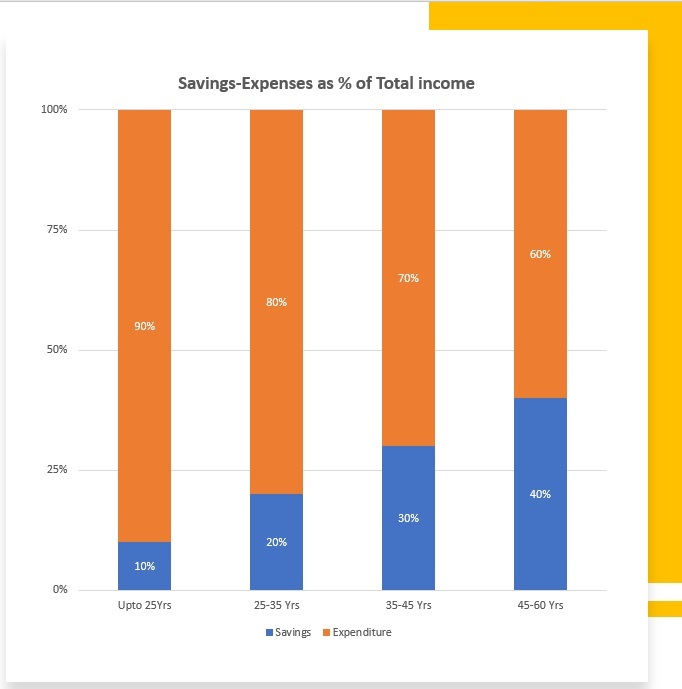

Savings is always a percentage of income. Savings should be residual of inflows left after expenses. Your investment goals (as per Box Framework) will determine the principal required for each objective. The plan should be to save enough to meet each of your goals and manage expenses from the balance. The below chart demonstrates the thumb rule of savings-to-income ratio (S2I ratio) at different stages of your life:

Target to save 10% of your income from an early age, as soon as you start to earn. Gradually your income increases, and you must double your S2I ratio. It is possible to double your savings % because your income grows in more proportion than expenses. Also, because you are likely to take on more responsibilities in life, increasing your savings is more relevant. In the 35-45Yrs age bracket, your income rises, and so does the financial liabilities. Still, again you must save enough to be able to save for your long-term financial goals.

Analyze the total expenditure

As a thumb rule, household expenses should be maximum of a third of your income. Specific expenses like tuition fees, medical and term insurance premiums are category by themselves. The idea is to measure the costs in each bucket to manage them better. Imperative to note this split is a guide is not sacrosanct. Income level, secondary income, education, background, parental asset, and liability help you decide the savings to income ratio that suits your circumstances.

Other factors to consider while making an investment plan

- Subscribe to medical insurance to reimburse you in case of eligible medical expenses. And term insurance, the purest and conventional form of insurance, pays the nominee a lump-sum or lump-sum + guaranteed income in case of death of the policyholder.

- Form a retirement corpus that is enough to earn you interest or dividend income or a combination of both to sustain your living expenses post-retirement. For the ones whose retirement is far away, consider inflation, family size, and rise in living expenses. Retirement planning is not about just fulfilling living expenses from interest & dividend incomes. The earnings can be from a combination of both the sale as well as revenue from an investment.

- Plan to purchase a house at a future date? Placed this objective in the relevant Box of the Framework, and consider the following points:

- Down payment and equity portion are required immediately at the time of purchase

- Plan for EMIs after adjusting income from that property, if any

- Restrict the EMI to income ratio to one-third as a thumb rule. Depending on your total family income, other assets, and liabilities, you can stretch the percentage to 40-50%

- Asset allocation is an important aspect, and equally important is how you invest in each asset class. Your ideal investment strategy should help you achieve the required diversification with minimum costs through vehicles (direct, indirect, advisors, etc.) that are sustainable.

To conclude

Individual circumstances and family background should determine your investments and savings. One size does not fit all, and therefore investment strategy is very personalized. Reference to inflows in the article refers to the income in hand (post-tax). Once you have started using these thumb rule, continue to review gaps to goals over time and rebalance as appropriate. Always trust your plan and remain consistent with your investment strategy.

——————————————————————————————————–

The author of this article is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity towards the subject of personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The article is based on the author’s knowledge, experience, and understanding of the subject. Any views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under no circumstances the author shall be liable for any views or analysis expressed in this note. Further, the views expressed are not binding on any authority or Court. Readers are advised to consult their financial advisor for advice for their specific case.

Excellent artical all in so much details that a person like me a senior citizen and non technical layman also read word to word carefully and planning for implementing the same…..great work Sagar ji….. congratulations.

Provide knowledge about investment strategy.

Nice and simply stated!

The article was wonderfully explained about savings and I think all young kids who started earning their living must read this thump rules.

I specially like the concept of S2I which really give insite of actual earning and saving ratio at different stage of life by consediring the various needs and goals of an individual.

Well explained and looking forward for more detail write-up on choosing righ asset class for diversified investment thump rules.

Nicely explained

very good article on financial planning.

I can just say those people don’t plan to fail, but they fail to plan.Good article Sagar, saving and investment is a habit gain through discipline.

Good one bro !

You can even start a youtube channel where you can start sharing it all in a presentation and video mode.

Really good one. Will await for further ideas from you.

Nice Article..

Explained the topic very effectively specially the concept of Income to Saving %, which is giving a great practical touch and understanding to the article. Saving is an important thing which needs to be planned by everyone honestly and firmly..

I understand saving % in the chart is minimum % which a person should plan for and the same can be increased with better planning and goals..