Financial planning is about wealth creation and having enough money for the non-earning years of life. Also, financial planning is about having money (and enough of it) when you need it. Therefore, it is essential to understand and follow the step-by-step process. But, of course, it is always easier said than done, especially for those who do not have a financial background or are new. So, here is a complete guide to financial planning for beginners.

The fundamentals of financial planning

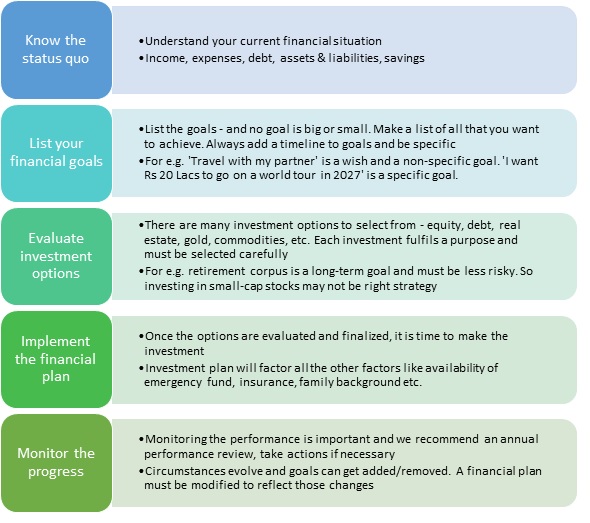

Financial planning is the step-by-step process to ensure you determine and meet the financial objectives. The plan helps you control your income and expenses and guides the monetary aspects of your journey. In other words, the process covers every possible factor that can economically affect you.

The focus is to save and invest with a long-term vision. Therefore, it would be best to consider all possible inflows (net of taxes) and outflows (recurring as well as non-recurring). Essentially, a well-drafted plan will lend you mental peace and ensure that you have funds when you need them.

What is the importance of financial planning?

- Helps deal with any financial emergencies

- It makes available the right quantum of financial assets, which provides mental peace

- Proper planning helps you avoid a debt trap

- Drives financial security

- A financial plan helps you derive a sense of satisfaction and achievement for all the hard work

- It helps create a robust retirement corpus so that non-earning years of life are tension-free

Remember:

No one can ever make a perfect plan, and no method is ideal. Furthermore, the idea is not to make a full-proof plan.

You have to start by determining the goals and begin your journey to chase them. Then, year after year, inch towards these objectives, which is the key to success.

No one is blessed to see the future. So if you are stuck with an immediate need or a roadblock you did not envisage, do not punish yourself or feel bad about it.

Just make a few adjustments and hit the road again. The most crucial aspect is to continue the investing journey. In other words, the idea is not to forecast roadblocks or avoid obstacles; it is about overcoming them when a calamity strikes.

Begin with the end – goal setting is the key

A clear understanding of the financial goals will help you use the available resources optimally. In other words, listing down specific goals upfront is the first step.

Time buckets

Split the goals into three different buckets – short term (within the next two years), medium-term (3-5 years) and long-term (beyond five years). The time buckets are suggestive. In other words, you can decide the duration based on your assessment.

Further, there will be goals that you can place in any of the two buckets. For instance, replacing the existing car can be a short-term goal. Still, it can also be a medium-term goal if the existing one is in good working condition. There is no right or wrong answer, and placement of goals into buckets is an objective assessment. The time-based split helps you allocate resources and your investment accordingly. Like, you would never want to tag a long-term product with a short-term goal. Mapping goals to incorrect time buckets will lead to sub-optimal returns, and you run the risk of falling short of meeting the target.

Be specific

You have to be specific in goal setting. In other words, a non-specific goal is as good as no goal. For instance, to set an objective like ‘I want to save enough to fund my daughter’s education expenses’ is a meaningless goal. It does not answer many critical questions like:

- In which year do you require the money? Essentially, the assessment of time at hand is missing

- How much money is needed?

- Is this a single goal, or do you want to save for graduation, post-graduation, masters or all of them?

- Is it a one-time need or spread across multiple years?

Instead, the goal should read something like this –

Goal setting date – 1st January 2022

Goal – Save Rs30 lacs for my daughter’s post-graduate education, payable in three equal instalments, i.e. 1st January 2030, 2031 and 2032.

If you begin with a specific goal, the chances to achieve it are high. Clearly defined plans will factor in time, inflation impact, rate of return and a few scenarios on account of changes in these factors.

Importance of goal setting

Managing a wallet comes in handy when the goals are clear. We all know the rule of thumb is that expenditure = total income less planned savings. Unfortunately, people often interchange the placement of outflows and the amount to save, which is disastrous. The single biggest reason is that the quantum of savings is not defined. Therefore, there is no measure to know if the amount saved is good or not.

Determining the goals and the savings required to meet them is extremely important. First, the money at your disposal gets rationalized, pushing you to prioritize expenses. Secondly, any short-term temptation for an impulsive purchase gets curbed, or at least you think twice. And finally, there is an objective measure to gauge if the savings you make are adequate or not.

Other benefits are:

- Drafting goals makes navigation meaningful, and you need to know where you are going in the investment journey

- Having a plan brings clarity to your expense decisions

- Goal-setting helps you evolve and adapt to changing life circumstances

- A report card of performance vs goals always holds you accountable

- The focus is apparent and pushes you to do the right thing (financially)

- The process urges you to choose the best investment option and prioritize expenses

The elephant in the room – how to create a financial plan?

A financial plan aims to meet the financial goals and consider several factors. For example, investment options consider risk tolerance level, age, family background, liabilities, investment preferences, etc.

Do read my article on a step by step guide on how to make a financial plan by yourself. Here is a quick summary of how to go about putting your thoughts together while creating a financial plan:

Few tips as you make a financial plan:

- A financial plan is not to make quick money, get rich faster or reduce expenses. Instead, it ensures your money is safe, well-invested, and available to you when needed

- Be specific to determine your life goals

- Have reasonable return expectations from your investments

- Make a fair attempt to understand the monthly expenses

- Never ignore taxes, and plan them efficiently

Read about Top ten financial planning tips for the middle class in India, where we have further elucidated this topic.

Deploy risk-management tools to remain on track in the investment journey

Our primary objective is to be able to meet the defined goals. Therefore, as a prudent investor, it is imperative to assess the deterrents (or the risks) and circumstances that could prevent you from meeting your financial goals.

Proper planning to mitigate risks is immensely beneficial, and here are the suggestions:

Emergency corpus

Create an emergency corpus equal to 12-18 months of living expenses. Having this fund will relieve you from any immediate cash burden if an unexpected outflow occurs.

Life is full of uncertainties, and you need liquidity. The emergency fund will help you tide over circumstances like a temporary job loss, business slowdown, medical expense, etc. In addition, if you are the primary earning member, the need for such a resource will be even high if something unexpected happens.

Buy insurance

Subscribe to both Top Mediclaim Policy in India and term insurance. Mediclaim protects you against the medical expenses incurred on hospitalization or treatment of a medical situation. On the other hand, term insurance is the purest form of life cover and is the most conventional insurance product. Term insurance involves the payout of the sum assured as a lump sum in case of the insured’s death.

Avoid debt trap

Availing debt can be a profound way to upgrade lifestyle and fulfil dreams. If planned well, debt serves the purpose as desired. However, interest paid on debt can also be the most significant impediment to your financial progress. In other words, unplanned debt and interest can be a considerable deterrent that impacts savings.

Unless you can plan your leverage and use that to your advantage, the goal must be to avoid debt. Or, if you must take a long, then retire the debt (costliest first) as early as possible.

Retirement planning – it is far, but it is worth starting now

Retirement is a critical milestone. Remember that retirement happens for everyone, whether self-employed or in service. It may not be a day for the former but a phase when you hand over business reigns and stop actively participating. In the latter case, you know the day.

You will celebrate the day if you are well prepared for the next phase of life. For an important event like retirement, thinking and planning must start at the right time. In other words, the sooner, the better. Therefore, it is essential to know how to plan for retirement at 35, 30, or even before.

Honestly, in the ’20s or ’30s, retirement may look like a distant goal post. And to be fair, it is an alien subject to most people at that age. But, despite that, starting right after you begin your career is still the best strategy.

You will understand (eventually) that how an early start worked out in your favour. Power of Compounding Money helps you take the maximum advantage of compounding returns.

Do you still wonder why make a retirement plan at all? Why not take life head-on, and act as it happens?

Here are a few simple reasons:

- The fact that you will not work forever and the active income will stop one day should be the single biggest motivator

- You will need funds to be able to maintain your lifestyle post-retirement. Life expectancy is increasing, so you need even more money to be able to last longer

- Saving money is possible only until you are earning

- Retirement is the golden era of life, and you want the best out of those years

- Interest rates are coming down. To rely on just the interest income can be risky, and hence you must plan for more avenues to fund your life

- Living with children should be an option and not the only option – a financially secure retired life will provide you with the independence you deserve

- You must have the resources to contribute to society and support the cause you believe in

- Be the one in the family who is always available to help, emotionally, physically and most importantly, financially. That enables you to leave behind a legacy

Here are seven steps to follow:

Make full retirement contributions

Salaried investors can contribute to the provident fund (PF), which happens automatically as per the statute. Further, there are options to increase the retiral savings through investing in National Pension Scheme (NPS), Public Provident Fund (PPF) or Voluntary Contribution to Provident Fund (VPF), etc.

Self-employed investors should consider a Public Provident Fund (PPF) account. This savings option locks in money and earns a decent risk-free return.

Plan to own a house

Traditionally owning a house has been a priority in life. In other words, this recommendation would have been irrelevant back in the day. However, generations have changed, and so have the thoughts. Millennials often do not want to commit to costly and long-term decisions like buying a house. They instead would prioritize spending on travel, entertainment and leisure.

It’s a change in the thought process. The way of life is anyone’s personal decision, as long as that does not leave one vulnerable in the future years. Are you are among those who do not want to commit to a property purchase? If yes, at least you must plan for the resources if there is a need in the future.

Invest in equities to accrue a grander sum

Equities are relatively risky. But, a long term plan can help you manage that risk. Therefore, approaching equity investing via the mutual fund route is often recommended.

An age-based fund allocation approach usually works. The base assumption is that your risk tolerance is indirectly proportional to your age, i.e., as the age progresses, risk appetite decreases. Risk appetite does not necessarily reduce to NIL with age. Still, it is prudent not to allocate new investible funds into equities after attaining a certain age.

Maximize returns through compounding

The power of compounding is a straightforward yet powerful concept in investing. The compounding occurs through the reinvestment of income. In other words, income on investment gets reinvested. Further, it earns revenue, which continues until the original investment exists, creating an income loop.

Those who start soon gain significantly higher returns than those who begin later. And that the power of compounding Money.

Create a secondary source of income

Always plan savings as a percentage of total inflows. In other words, net savings should not be residual income after meeting household and entertainment expenses.

Further, invest the savings based on the investment objectives. The income generated from investments is called secondary income. Therefore, your focus should be to develop secondary sources of income.

Keeping money idle in the savings bank account is a criminal waste of opportunity. Although it sounds trivial, income from idle money could add up to a significant amount over the years if invested in a liquid or debt fund.

Plan your leverage

Debt is famous, but the interest paid is pure cost and impacts savings. However, with proper financial planning, you can take leverage and use it to your advantage and create wealth.

Believe in investing

The attempt is to continue to increase income each passing day. There are two ways –

- improve the direct revenue, or say, the primary source of income

- invest wisely to enhance the passive income

Never hesitate to start with whatever little you have. A Systematic Investment Plan (SIP) is a great way to start investing small and regular.

Choose wisely amongst the asset classes and diversify the investments. To minimize risk and time investment, go via the mutual fund route. Investing in mutual funds is a reasonably straightforward process. Every investor can find investments that suit their requirements.

The Indian perspective:

Financial awareness is low in India for historical reasons. The earlier generations did not prefer to involve the younger generation in discussions related to money. Maybe, they were right, and the approach made sense then. But the times are changing now, faster than ever.

More nuclear families lead to decentralized decision making. A growing middle class, higher level of education, and the more need for resources increase the need for financial planning. Improving life expectancy due to better standards of life, technological advancements in medical sciences demands better insurance coverage, larger retirement corpus.

Employers are reducing the terminal benefits and shying away from defined benefit plans. That makes it critical for people to adopt sound financial planning, mainly because India does not offer good social security. There are systems and schemes available, but those are not enough.

The bottom line regarding financial planning for beginners

Financial planning is like navigation when you drive. If you know the destination and the road leading there, reaching there becomes easy. The challenge arises when you are unaware of the endpoint or the goal.

The process can be elaborate, but the outcome will be rewarding if you follow the proper procedure and possess an optimistic mindset. You do not have to be visionary but certainly need some financial acumen and appropriate behaviour.

Taking professional assistance is an option

Indian investors often shy away from engaging with experienced financial planners. There are many possible reasons.

First, there is a lack of conviction to seek professional advice as investors do not see enough value. Second, people do not believe that a financial plan or an expert can create value. Finally, paying fees for a piece of financial advice not backed by guaranteed returns is often unacceptable. Nevertheless, society is evolving, albeit slowly, and we see more demand for professional guidance in India.

In conclusion, forming a financial plan is a necessity. Further, building a financial plan by yourself is a possibility. As an investor, you will see the value of a financial plan over time. So give it time. Proceed with the firm belief that a financial plan creates value and keep faith in this wealth creation process.

Happy financial planning!

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. The author wants to share his knowledge and understanding of the subject through his writing.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme caution to avoid possible mistakes. However, the author does not take responsibility for any error that exists.

The article’s views, opinions, and thoughts belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.