How to plan long-term savings and manage expenses wisely? Questions like these are pretty common in everyone’s mind. Needless to say that everyone, and I mean everyone, has to prioritize saving money for the future. If you do not save enough, you will struggle in the long term.

Traditional saving options like mandatory retirement savings and pensions are usually not enough to sustain. One assumption is that the progress in life reflects in our routine. Social security is still evolving in India and may turn out to be insufficient when the time comes. After all, stripping the style from our lifestyle is not aspirational. And therefore, you must plan for long-term savings.

What are we trying to achieve?

Make suitable investments and have long-term savings. Clearly defined financial objectives and the net savings required to meet those goals is essentially the start line. Next is investing those savings into assets that grow and eventually help achieve those objectives (say the finish line). Finally, investment choices consider factors like the return on investment, taxes, asset risk, etc. Now, this seems pretty straightforward, which in most cases is not the case. In other words, there are multiple options to evaluate, many scenarios to consider before one can make a savings plan.

What are the various asset classes to consider?

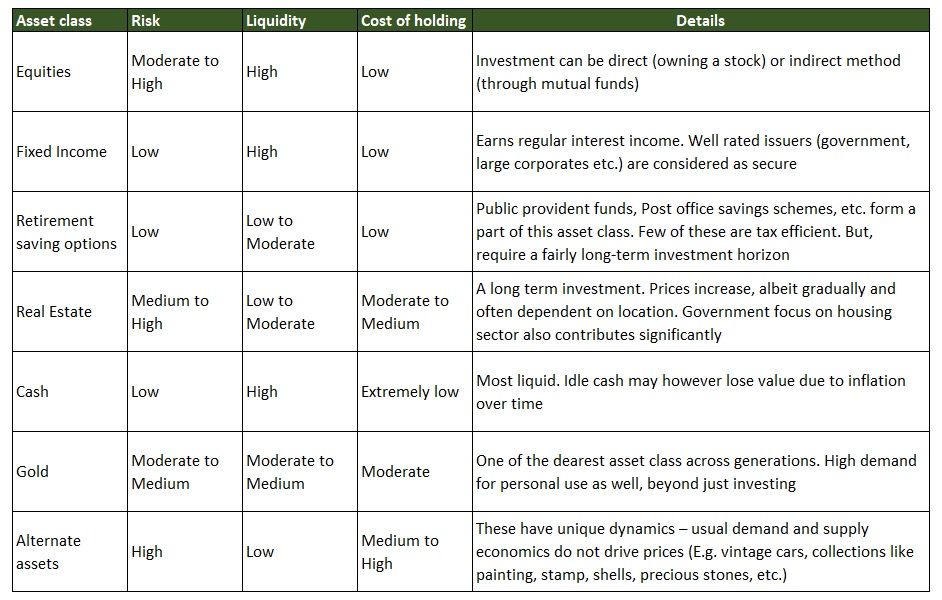

There are several asset classes and sub-classes for each one of them. Investors with varying risk profiles should consider the assets based on their risk profile and time horizon. Below are various asset class options.

Points to note to understand the table:

- Scale in the above follows this sequence: Low–Moderate–Medium–High

- Liquidity is the ease and ability to convert the asset into cash or equivalent. High liquidity is easiest to convert

- The cost of holding is the financial impact to manage and maintain the asset

Long-term savings and investment plans are vital for a secure future. Without a well-funded retirement corpus, either you will struggle to make ends meet or work for an extended number of years. Unfortunately, both options are not peaceful.

To retire and enjoy the remainder of life, you must follow a systematic approach towards a retirement plan. Read here to understand what retirement planning is and a step-by-step guide to the same. Here are the most critical and time-tested long-term saving ideas. (not in the order of importance)

Idea #1 – Create an emergency corpus

An emergency corpus will serve you well at the time of an unexpected outflow. Life is full of uncertainties, and you need liquidity to tide over stressful situations like job loss, business slowdown, medical expense, etc.

In case you are the primary earning member, then the need for such a fund is immense. After all, there is limited scope to downsize the fixed household expenses temporarily.

Emergency Corpus = 12 to 18 months of living expenses.

A survey conducted by Spending Behaviour in India shows 60% of Indians have less than Rs 5,000 in their savings. Moreover, almost 90% of young Indians have less than Rs 25,000 in their emergency fund. That is an alarming statistic, and you must create an emergency corpus.

Idea #2 – Avoid debt, and if not possible, then pay off on a priority

At first, avoid debt to upgrade lifestyle and buy fast depreciating assets (like consumer durables). Many of you may not recon with this recommendation and rather believe on the contrary. Debt brings along interest cost, which is avoidable. In other words, one should only spend as much as one can afford.

Interest cost can impede your financial progress. While a well-executed debt can serve the desired purpose, an unplanned obligation can be a considerable deterrent affecting savings. Therefore, use debt to your advantage if you cannot avoid it.

To conclude, the goal is to prevent debt in the first place. But if that is not possible, retire debt as early as possible, starting with the costliest first.

Idea #3 – Create a Retirement Corpus

The retirement corpus will be very different for every individual. Several circumstances determine the amount, and therefore it is an art to figure out a suitable target. In other words, a close look at your lifestyle, family background, dependents, etc., will help you reach a ballpark number.

Since the process is hypothetical, never judge the number. Target is always notional, based on certain known factors. Your inner wisdom, your gut feel, will tell you if the number is enough or not.

Once you have the target number, start saving and investing immediately to ensure you reach the destination.

Read about how much do you require to retire here.

Idea #4 – Save to buy a house

House is an essential asset and often indicates social progress and well-being. The idea is to have a house to live in eventually when you need it.

The location where to buy a house is critical. It may be worth noting that workplace cities are often not the final destination. Based on your circumstances, you can decide where you would like to buy or rent a house in the work city.

There are advantages to buying a house early in your career. First, you get more time to pay off the loan. Second, the tax benefits on interest and principal loan payment encourage people to invest in a house. Finally, capital appreciation can be remunerating over a long duration.

The flip side is that the loan eligibility is low at the start of the career. In other words, buying a house that can serve future needs may not be possible. However, trading a smaller home for a bigger one with incremental investment is a possibility.

If you want to buy a house later, then you must save for the down-payment. The more savings you have, the lower the mortgage and hence lower the liability later. Alternatively, you must save for the differential payment if you plan to move from a small to a bigger house.

Idea #5 – Contribute to retiral benefits

The idea here is to continue to save for the long term. You can choose the form and format, but continuous savings is the actual intent. There are several options like mutual funds or direct equity investing. Similarly, traditional instruments like the PF/PPF are also an excellent choice. Also, investing in infrastructure bonds, etc., is a possibility.

For salaried investors, contribution to provident fund (PF) happens as per the statute. Further, there are options to increase the retiral savings through investing in National Pension Scheme (NPS), Public Provident Fund (PPF), or Voluntary Contribution to Provident Fund (VPF), etc.

Self-employed investors should consider opening a Public Provident Fund (PPF) account. The option locks in money and earns a decent risk-free return.

Forcibly saving money also prevents any unjustified spending and eventually contributes to retirement goals.

Idea #6 – Create a secondary source of income

Steadily, you will make investments as per the investment strategy. Gradually those investments will begin to generate income. That is called secondary income. The focus should be to develop more and more such sources of revenue.

Secondary income means the income generated from your investments.

Follow the golden principle, increase your savings, and reduce debt. The attitude fits in the strategy to increase income from savings and lower interest costs.

In the words of legendary investor Warren Buffett, only multiple income sources can lead to financial independence. An investor has done injustice if there is no secondary income source by the age of 45. A lot depends on when one starts, and the focus is not whether 45 years is the right age.

The focus is on the concept that one should develop multiple sources of income as soon as possible. Do read about financial freedom here.

Idea #7 – Save for significant events in life

Our lives are full of events, some known and welcome while few unsolicited and unwanted. There is one common thread, and that is the need for money.

In other words, the demand for money is constant. If the financial position is stable, you can enjoy all the events of life. If you have not planned, overcoming an unwelcome event can be painful. While there is little you can do to avoid an unsolicited event, you can still plan your savings to help you overcome such circumstances.

So what’s the best way forward? Plan for all the significant events, good or bad. And save for the unsolicited ones. Below is the list of a few events that you should consider:

- Marriage expenses

- Buy (or upgrade) a car or other depreciating assets

- Cost of higher education for children

- Medical expenses

- Travel expenses

- Any loss of income or ability to earn, temporary or permanent

Timely planning and saving for all the major life events will help you avoid a crisis.

Idea #8 – Buy a Mediclaim and Term insurance policy

A Mediclaim policy is insurance against the medical expenses incurred on hospitalization or treatment of a medical situation. The Mediclaim policy covers:

- Hospitalization expenses

- Treatment of critical illnesses

- Medical costs incurred pre and post hospitalization

- Specified day-care treatments

Mediclaim is for a defined period and requires renewal. Read more about the Mediclaim policy here.

Term insurance, the purest form of life cover, is the most conventional form of insurance. Return of term insurance involves payout of the sum assured as a lump sum in the insured’s death.

As a result, people seldom get confused about the utility of life insurance. The return is the lump-sum payment received in case of the death of the policyholder. In other words, if the policyholder outlives the policy tenure, there will be no return.

Above all, the idea here is not to earn. Instead, the objective is to secure the family financially. Therefore, the amount of term insurance depends on several factors. Read more about how much term insurance is required.

Start early to gain maximum from compounding returns

Early investors achieve the full advantage of the power of compounding returns. It is a straightforward concept but highly critical.

The compounding occurs through the reinvestment of income. Income from investments is reinvested and further earns income. This sequence continues until the original investment exists.

The time duration of investment plays a critical role. In other words, an extended period allows maximum compounding and therefore multiplies the returns. The power of early investing is well-covered with instances in the earlier article.

How to manage expenses wisely?

We must keep in mind that resources are finite. And never take the availability of money for granted. After all, if the inflows were unlimited, the approach will be very different.

Therefore, here are some critical tips for managing your wallet. Always remember that expenses must be the residual of income after making the required savings and investments.

For that to be true, you must manage an essential factor, i.e. the expenses. Expense management is essentially getting the correct value in return for every penny spent. And here are some vital tips:

- Know your outflows – always split them into discretionary and non-discretionary. You do not want to curb expenses right away, but the distinction helps

- Have a budget – not a one with every detail, but ballpark numbers are enough. Like your credit card invoice is always in a particular range. If it is not, you must know why and more than often, it helps

- Try to get the best deal – this applies to every outflow. For instance, travel expenses, entertainment costs, buying a piece of furniture, etc. In the end, cumulative savings will add up to a handsome amount

- Be cautious while buying luxuries and avoid an impulsive purchase. Never try to create an impression by showing off fancy stuff. Generally, it doesn’t work that way, and such an approach causes more harm than benefit

- Use credit judiciously – especially in today’s world where plastic money is highly prevalent and availing credit is comparatively easy. Be sensible and think twice before you swipe your card

Treat yourself, but be prudent. After all, the idea is not to cut down on things that bring you delight. Instead, the intention is to curtail any unnecessary splurge. Reward yourself and your family with gifts, vacations and spend wherever you find moments of joy.

Create a budget and use it as a guide

It’s not always the same tedious exercise of listing expenses line by line. The idea is to make sure that you have thought after your outflows according to your income. After all, it is the value that you derive from the budget that matters and not the process of creating one. Once you have the perimeter in place, use that as a guide.

To be good with money takes time and practice. Gradually you will get used to planning well and planning ahead of time. For instance, you will push off some purchases until you cannot afford them once you decide based on circumstances. The more you make money managing a habit, the better will be your financial life.

The bottom line on how to plan long-term savings

Savings help you get the funds when you need them. Focused efforts help you grow savings.

Long term savings is simple to follow but not easy to achieve. Achieving success requires discipline, proper planning, tight execution and systematic review of progress. Never overreact to any temporary situation and always have patience.

First, split the investment horizon into short, medium and long-term. That will allow you to process the investments in the right light.

Second, work upon and implement an investment strategy suitable to the horizon.

Third, take appropriate risks. Diversify your portfolio and distribute risks, but taking less risk will lead to compromise on returns.

Fourth, remember that you must beat inflation. The longer the duration, the higher the need to manage the loss of value due to inflation.

And lastly, make goal-based plans to ensure you do not compromise on targets and you do not have to mix the purpose.

Remember that every penny counts. Always value savings more than products. Happy investing!

About the author

The author is a senior finance professional with over fifteen years of work experience in corporate finance. He has an affinity for matters relating to personal finance and investment management. Through his writing, the author wants to share his knowledge and understanding of the subject.

Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer

The author has used his knowledge, experience, and understanding of the subject and has exercised extreme care and caution to avoid any possible mistakes. However, the author does not take any responsibility for any error that exists.

Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

Explore Best Long Term Savings Plan With us. Secure your Financial Future with Long Term Savings and Personal Expense Management.