Don’t Put All Your Eggs in One Basket. Heard of it? Great, then you are half-way through. What that means in an investment context is to never concentrate your resources in one place. By that, you significantly increase the risk of losing all. Half glass full, that also means you have an opportunity to mint substantial gains if the value increases multifold. Unfortunately, that is not how you make an investment strategy and therefore it is important to know major asset classes for portfolio diversification.

What is asset allocation?

Asset allocation is to translate this understanding into practice. Following an allocation strategy will help you split investments into eligible asset classes. Each asset class has a unique return and risk profile. An allocation strategy will help you maximize returns by optimizing risks. The attempt is to split into asset classes that have low correlations. Simply put, the value of these assets generally does not move in the same direction, which provide a hedge and reduce the volatility of returns.

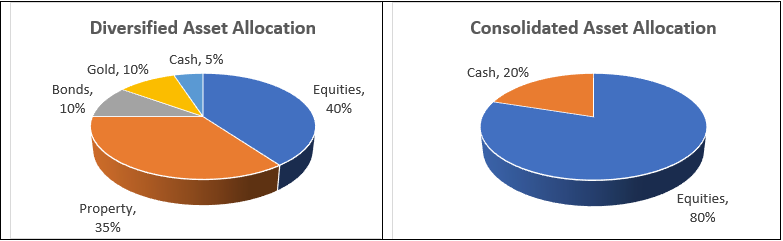

Below are two broad examples of allocation strategy – diversified or consolidated.

Splitting investible surplus into the different asset classes is called diversification. The attempt here is to limit losses, reduce return fluctuations, and still grow the investment value. Diversification has a direct bearing on the ability to meet your financial objectives. It is not always about minimizing risk; rather it is about optimizing risk to help you achieve goals as per the Box Framework.

Read more about the box framework in my article here – https://decodefinance.in/finance/thumb-rules-of-financial-planning/

Asset classes and their key characteristics

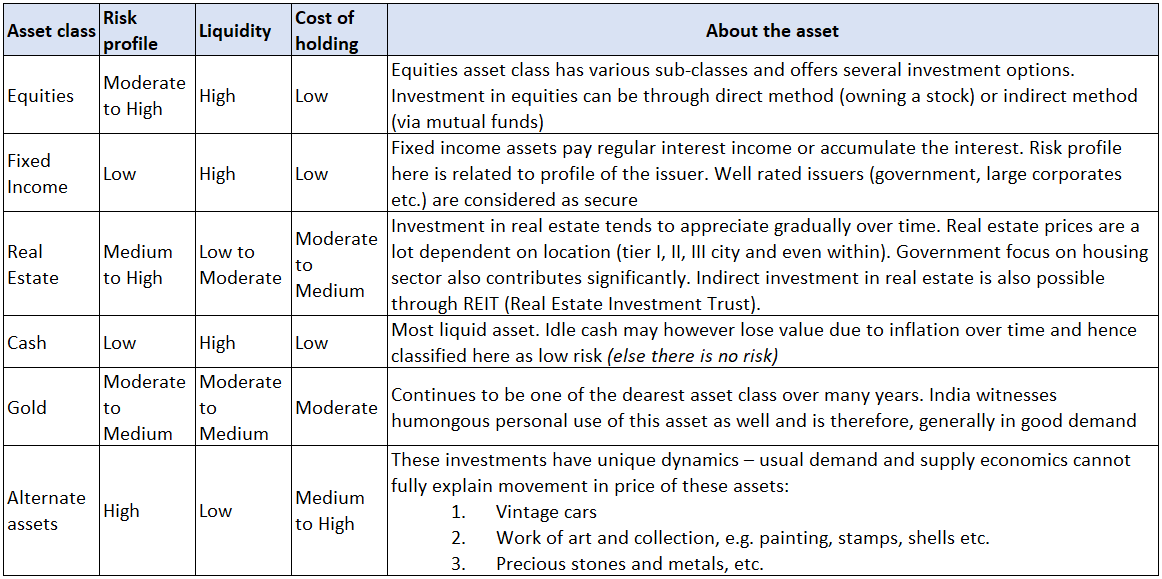

Here are some of the important asset classes and their key characteristics. The asset profiling is for a median income-earning middle-aged investor who has a long-term investment horizon. These characteristics may be considerably different for a different investor profile.

- Scale for the measure in the above follows this sequence: Low–Moderate–Medium–High.

- Liquidity is defined as the ease and ability to convert the asset into cash or equivalent. High means asset can be converted into cash almost immediately

- Cost of holding is the financial impact to manage and maintain the asset class

What is not included?

Statutory contribution to Provident funds, state funds, and equivalent schemes is an investment class by itself. A significant portion of these contributions is mandatory, though there can be some degree of flexibility. Since this investment class is primarily regulation-driven, we have excluded them from the above table.

Allocation is situational

It is imperative to note that risk is individualized and relative to your situation. Factors like existing assets and liabilities, commitments, age, income, etc. play a critical role. There is no formula to derive an optimal asset allocation. To be able to properly allocate investments is one of the most critical decisions in the investment journey. Asset allocation strategy should coincide with your investment objectives keeping in mind the constraints.

Example:

Consider you have a short-term goal to pay Rs10 Lacs for a child’s college fees after 1.5-years. This is a non-flexible goal and you cannot take any risk. Here are the investment options you have:

- Go for a conservative approach and keep Rs10 Lacs in cash (or equivalents). Extremely liquid and risk-free, but there is an income opportunity lost

- Invest in fixed income (e.g. bonds). Reasonably secure and earn in the range of 7-9% p.a., so you must invest about Rs8.5Lacs. This investment is liquid as well as secure

- Purchase of gold or property is not advisable in this situation since these long-term investments. Also, risk tolerance is low for this goal and these assets are considered risky

- Whether you invest lump-sum or gradually, arriving at the decision will follow the same assessment process

How much should you invest in equities?

Equity is considered a volatile asset class. One question keeps many puzzled – how much should I invest in equities? Since investment into equity is simple from an execution perspective, it is important to draw a line and know your limits. Following an age-based approach which essentially assumes that your risk tolerance is indirectly proportional to your age can be worth considering:

The proportion of your investment into equity = 2times the balance earning years

| Age of investor | Earning years left (assume up to 65years is the earning age) | Proportion of equity investment (2X earning years) |

| 25yrs | 40yrs | 80% |

| 35yrs | 30yrs | 60% |

| 50yrs | 15yrs | 30% |

| 65yrs | — | — |

Risk appetite does not necessarily reduce to NIL as you age, but it is prudent to minimize allocating new investible funds into equities. In the case of a self-employed investor, you must boil down on an age up to which you can work full steam.

Based on your goals and objectives, the balance investible surplus should be split into other asset classes. Another common trend is to invest in gold.

Do not let the recent performance influence allocation strategy

In general, investment decisions are taken to serve financial goals over long term. The performance of an asset class is dependent on factors like the state of the economy, political stability, and many global factors. Based on your goal, undue importance to the recent performance may lead to a suboptimal allocation strategy.

Take a recent example wherein after the national lockdown was announced in India, equities got significantly hammered while gold gained. If you have a long-term view, this blip can be an investment opportunity rather than a panic situation. Hence, never let any temporary phenomenon or fear influence your long-term strategy.

Other factors affecting decision

Several other factors influence asset allocation decision, for instance:

- Goals – the flexibility of goals allows you to better diversify depending on your risk appetite

- Risk tolerance – optimize risks based on the expectation of returns

- Financial situation – your financial background as an individual & as a family is critical

- Time horizon goes hand in hand with your goals

- Constraints – choice of asset class (e.g. equity is an asset class) or subclass (e.g. small-cap stocks within equity) also play an important role

- Age is an important factor in determining the risk profile

The objective of allocating investible surplus into different asset classes is to hedge risks through diversification. However, the fundamentals of investment philosophy i.e. to have patience, to take calculated risks, and to invest consistently always hold.

——————————————————————————————————–

The author of this article is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity towards the subject of personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The article is based on the author’s knowledge, experience, and understanding of the subject. Any views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under no circumstances the author shall be liable for any views or analysis expressed in this note. Further, the views expressed are not binding on any authority or Court. Readers are advised to consult their financial advisor for advice for their specific case.

Learn about investment portfolio diversification with Us. Explore asset allocation strategies and portfolio diversification examples to optimize investments

I guess its a great insights for people who wants to invest and also for those who are already in it can re-visit to minimise risks and maximise returns. It would be great if you can explain what is Mutual funds, equity, bonds and gold in investment contexts which will help us who don’t understand this domain.

Good work and keep educating us.

Nice article which give lots of clarify specially younger people as to how to create their asset portfolio in more systematic and scientific way.

very useful and important teaching of finance management

Good going. Keep it up.

The current FD rates are gone down to 5% now, but still prefer to go for it, as in the current scenario be it mutual funds or shares, both are down.

Content help to understand the issue.