What is Planning? It means what we decide today in advance for future events. The process starts with predetermining the events, defining objectives and careful planning to achieve those aims. Financial planning is similar and an extension of the concept, just that the scope is money-related. We will elucidate how to determine the money goals and focus on the importance of financial planning in India.

What is financial planning?

Financial planning is the step-by-step process to ensure you determine as well as meet the financial objectives. The plan helps you control your income and expenses and acts as a guide in your life journey. The process covers every possible aspect that can economically affect you, as listed below.

The focus is to save and invest with a long-term vision. The plan considers total inflows (net of taxes) and all the outflows (recurring and non-recurring). One must pay for household expenses, meet life goals, pay insurance premiums, etc. and still save for retirement corpus. A well-drafted plan will lend you mental peace and ensure that you have funds when you need them.

Assume you have an objective to fund a child’s college fees of Rs 10 Lacs after eight years. The financial plan will guide you to achieve this objective. The need here is time-sensitive, and risk tolerance is minimal. You can expect answers to questions like, 1) How much should you save to meet this outcome?, 2) Where should you invest these funds?, 3) Which investment options should you consider? Etc.

How to create a successful financial plan?

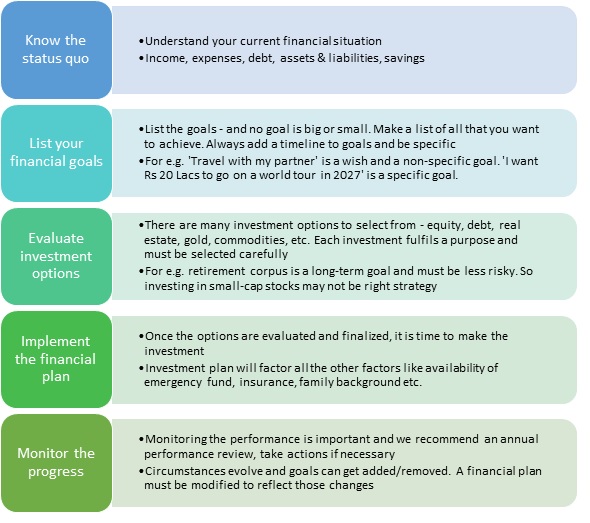

A financial plan aims to meet the financial goals. Investment options consider risk tolerance, factors like age, family background, liabilities, and specific investment preferences.

Here is a guide on how to create a financial plan:

Split the objectives into phases

Firstly, split the financial objectives into three phases:

- Short-term goals like pay-off an expensive debt (e.g. a personal loan), create an emergency fund, make a monthly expense budget etc.

- Medium-term objectives, e.g. buy life insurance policy, subscribe to health insurance, down-payment for a home loan, pay off a home loan, children’s education fund, etc.

- Long-term target, which is primarily about the retirement and estate planning

Secondly, understand the nuances of every goal within each phase. These include risk tolerance, flexibility on the amount, time sensitivity, etc.

And finally, make a focused investment plan for every specific goal.

Few tips to know as you make a financial plan

A financial plan is not to make quick money, get rich faster or reduce expenses. It is to ensure your money is safe, well-invested and is available to you when needed. Ultimately help you lead a stress-free and comfortable life.

Here are a few tips as you draft your financial plan:

- Be specific to determine your life goals

- Have reasonable expectations from your investments

- Understand your monthly expenses

- Form an emergency fund

- Purchase a Health and life insurance policy

- Plan your taxes efficiently

Read further about the ‘Top ten financial planning tips for the middle class in India.‘

What are the key objectives of financial planning?

The most important question under consideration is – what is the primary goal of personal financial planning? Here are the key objectives of a financial plan:

- Determine the right savings amount and make suitable investments

- Empower you to enjoy and maintain a good standard of life

- Be prepared to withstand financial emergencies

- Witness wealth creation and leave a legacy for family

- Ensure you have money when needed

- Attain peace of mind

- Manage your money and serve the society

- Avoid any unnecessary debt

Also, read about the importance of saving money for the future here.

Importance of financial planning in India

One can never ignore the importance of financial planning and the exercise is more than just reducing or tracking expenses or improve savings.

A financial plan is about being futuristic. It is to identify financial goals and to determine the means to fulfil them. Some of the most important advantages are listed below:

Deal with a financial emergency

A good start would be to create an emergency fund to help you deal with financial trouble during an unfortunate event. The majority of your costs remain the same during distress times (e.g. a job loss). This emergency fund will help meet those immediate financial needs. Living expenses to survive for 12-18 months should be the size of the emergency corpus.

Financial assets lend mental peace

Our lives are full of events, and the demand for money is constant. If your financial position is stable, you can peacefully skit through such unwanted events and with lesser pain.

The best would be to plan all the significant events, good or bad. But that is practically impossible. In the absence of any such conclusive list of life events, here is a guide to put you in the right direction:

- Marriage expenses

- House purchase

- Buy (or upgrade) a car

- Cost of education

- Medical expenses

- Dream vacations

- Loss of income or ability to earn

Timely planning and saving for these events will help you avoid a crisis.

Avoid a debt trap

A situation of distress may drain financial resources. To fulfil any fund shortage, one may seek a personal loan or use a credit card beyond paying capacity. The debt trap begins small. But if not managed well, a severe debt trap is created you realize when it is often too late. A sound financial plan will consider distress scenarios.

Drive financial security

Financial resources do give strength to deal with the situation even if they cannot lower the adversity. Also, growth in savings and investments makes you feel compensated for your hard work.

Once you start to plan expenses based on your income, saving money is a natural outcome. To get into this rhythm may take some time and practice. However, eventually, the savings and investing process becomes natural to you. Saving money will help you leave a legacy and wealth for future generations.

Create a retirement corpus

Retirement planning is a critical aspect and must form part of a well-rounded financial exercise.

The objective is to be able to enjoy the post-retirement phase through sound financial planning. This non-compromising goal considers all reasonable aspirations and matches them with economic realities. One must apply a step-wise approach to determine the target corpus.

At this link, you can also read about ‘how much money do you require to retire.‘

Importance of financial planning in the Indian context

Financial awareness is very limited in India for historical reasons. The earlier generations did not prefer to involve the younger generation in discussions related to money. Maybe, they were right, and the approach made sense then.

But the times are changing now, faster than ever. More nuclear families lead to decentralized decision making. A growing middle class, higher level of education, and the more need for resources increase the need for financial planning. Improving life expectancy due to better standards of life, technological advancements in medical sciences demands better insurance coverage, larger retirement corpus.

Employers are reducing the terminal benefits and shying away from defined benefit plans. That makes it critical for people to adopt sound financial planning, mainly because India does not offer good social security. There are systems and schemes available, but those are not enough.

mindset on financial planning

Indian investors often shy away from engaging with experienced financial planners. There are many possible reasons.

Firstly, there is a lack of conviction to seek professional advice as investors do not see enough value. Secondly, people do not believe that a financial plan can really create value. And finally, paying fees for a piece of financial advice not backed by guaranteed returns is often not acceptable.

However, society is evolving, and we see more demand for professional guidance in India as well.

The bottom-line

Financial planning is a great way to achieve mental peace and can be an excellent source of motivation. A carefully drafted plan reduces the uncertainty and supports you at the time of need.

No one can ever make a perfect plan, and no method is ideal. The idea is not to make a full-proof plan.

You have to start by determining the goals and begin fast to chase them. To inch towards these objectives linearly, year after year is the key.

Life is uncertain, and no one is blessed to see the future. If you are stuck with an immediate need or a roadblock you did not envisage, do not punish yourself or feel bad about it.

Just make a few adjustments and hit the road again. Most important is to continue the journey. The plan is not to forecast or avoid obstacles; it is about overcoming them as soon as possible.

As easy as it may sound, the process is lengthy and quite elaborate. Setting up goals, finding the right avenues to invest, forecasting the periods when you may require money, etc., is not straightforward. You do not have to be visionary, but you need elementary (or a bit more) financial understanding to create a successful financial plan.

Financial planning is like navigation. If you know where you are and where you want to reach, navigation becomes easy. The challenge arises when you do not know the answer to one or both of these questions.

Do not hesitate to speak with your financial planner and seek assistance. A short-lived financial plan is worthless, and you must take all possible efforts to succeed in this effort.

The author is a senior finance professional with over fifteen years of work experience in corporate finance and has an affinity for personal finance and investment management. Please leave your comment or share thoughts on this article via email at decodefinance.in@gmail.com. For more articles, please visit the website www.decodefinance.in.

Disclaimer:

The author has used his knowledge, experience, and understanding of the subject to write this article. Any views, opinions, and thoughts mentioned in the article belong solely to the author and not necessarily to the author’s employer (past or current), organization, committee, or other group or individual.

Under any circumstances, the author shall not be liable for any views or analysis expressed in this note. Further, the opinions expressed are not binding on any authority or Court. We advise readers to consult their financial advisor for assistance in their specific case.

We Explain The importance of financial planning with guidance. Learn What Is personal financial planning and Concept Of Financial Planning.